静态效果图:

第一部分获取龙虎榜大券商的持仓数据,包括:

成交量,多仓,空仓;

第二部分plotly画图,取两个代表性的期货尚

中信和国泰君安(多空差较大)

plotly图像丰富,只能保存网页html格式或静态图片

#1获取数据

from jqdatasdk import *

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import matplotlib.mlab as mlab

import matplotlib.ticker as ticker

plt.style.use("ggplot")

import talib

#解决中文显示问题

plt.rcParams['font.sans-serif']=['SimHei']

plt.rcParams['axes.unicode_minus'] = False

auth('','')

b1 = []

b2 = []

b3 = []

b4 = []

b5 = []

b11 = []

b12 = []

b13 = []

b14 = []

b15 = []

b21 = []

b22 = []

b23 = []

b24 = []

b25 = []

b31 = []

b32 = []

b33 = []

b34 = []

b35 = []

c1=[]

c2=[]

c3=[]

c4=[]

c5=[]

c11=[]

c12=[]

c13=[]

c14=[]

c15=[]

c21=[]

c22=[]

c23=[]

c24=[]

c25=[]

c31=[]

c32=[]

c33=[]

c34=[]

c35=[]

d1=[]

d2=[]

d3=[]

d4=[]

d5=[]

d21=[]

d22=[]

d23=[]

d24=[]

d25=[]

d31=[]

d32=[]

d33=[]

d34=[]

d35=[]

d11=[]

d12=[]

d13=[]

d14=[]

d15=[]

price=get_price('IF1906.CCFX',end_date='2019-05-17',count=22)

#501001-成交量排名, 501002-持买单量排名, 501003-持卖单量排名

date=['2019-04-15', '2019-04-16', '2019-04-17', '2019-04-18', '2019-04-19',

'2019-04-22', '2019-04-23', '2019-04-24', '2019-04-25', '2019-04-26', '2019-04-29', '2019-04-30',

'2019-05-06', '2019-05-07', '2019-05-08', '2019-05-09', '2019-05-10', '2019-05-13', '2019-05-14',

'2019-05-15', '2019-05-16','2019-05-17','2019-05-20']

# 501002-持买单量排名

for k in date:

q=query( finance.FUT_MEMBER_POSITION_RANK.day,

finance.FUT_MEMBER_POSITION_RANK.code,

finance.FUT_MEMBER_POSITION_RANK.rank_type_ID,

finance.FUT_MEMBER_POSITION_RANK.rank,

finance.FUT_MEMBER_POSITION_RANK.member_name,

finance.FUT_MEMBER_POSITION_RANK.indicator,

finance.FUT_MEMBER_POSITION_RANK.indicator_increase,).filter(

finance.FUT_MEMBER_POSITION_RANK.code=='IC1906.CCFX',

finance.FUT_MEMBER_POSITION_RANK.rank_type_ID=='501002',

finance.FUT_MEMBER_POSITION_RANK.day==k).order_by(

finance.FUT_MEMBER_POSITION_RANK.member_name.desc())

df=finance.run_query(q)

for i in range(len(df)):

a = "中信期货"

if a in df.loc[i, 'member_name']:

a1 = df.loc[i, 'member_name']

a2 = df.loc[i, 'indicator']

a3 = df.loc[i, 'indicator_increase']

a4 = df.loc[i, 'code']

a5 = df.loc[i,'day']

b1.append(a1)

b2.append(a2)

b3.append(a3)

b4.append(a4)

b5.append(a5)

print(b1)

for ii in range(len(df)):

a = "海通期货"

if a in df.loc[ii, 'member_name']:

a1 = df.loc[ii, 'member_name']

a2 = df.loc[ii, 'indicator']

a3 = df.loc[ii, 'indicator_increase']

a4 = df.loc[ii, 'code']

a5 = df.loc[ii,'day']

b11.append(a1)

b12.append(a2)

b13.append(a3)

b14.append(a4)

b15.append(a5)

for iii in range(len(df)):

a = "国泰君安"

if a in df.loc[iii, 'member_name']:

a1 = df.loc[iii, 'member_name']

a2 = df.loc[iii, 'indicator']

a3 = df.loc[iii, 'indicator_increase']

a4 = df.loc[iii, 'code']

a5 = df.loc[iii,'day']

b21.append(a1)

b22.append(a2)

b23.append(a3)

b24.append(a4)

b25.append(a5)

for iiii in range(len(df)):

a = "华泰期货"

if a in df.loc[iiii, 'member_name']:

a1 = df.loc[iiii, 'member_name']

a2 = df.loc[iiii, 'indicator']

a3 = df.loc[iiii, 'indicator_increase']

a4 = df.loc[iiii, 'code']

a5 = df.loc[iiii,'day']

b31.append(a1)

b32.append(a2)

b33.append(a3)

b34.append(a4)

b35.append(a5)

f1 = pd.DataFrame(columns=['day', 'member_name', 'indicator','indicator_increase'])

f1['day']=b5

f1[ 'member_name'] = b1

f1['indicator'] = b2

f1['indicator_increase']=b3

f1 = f1.set_index(['day'])

f11 = pd.DataFrame(columns=['day', 'member_name', 'indicator','indicator_increase'])

f11['day']=b15

f11[ 'member_name'] = b11

f11['indicator'] = b12

f11['indicator_increase']=b13

f11 = f11.set_index(['day'])

f21 = pd.DataFrame(columns=['day', 'member_name', 'indicator','indicator_increase'])

f21['day']=b25

f21[ 'member_name'] = b21

f21['indicator'] = b22

f21['indicator_increase']=b23

f21 = f21.set_index(['day'])

f31 = pd.DataFrame(columns=['day', 'member_name', 'indicator','indicator_increase'])

f31['day']=b35

f31[ 'member_name'] = b31

f31['indicator'] = b32

f31['indicator_increase']=b33

f31 = f31.set_index(['day'])

#501003-持卖单量排名

for i in date:

q=query(finance.FUT_MEMBER_POSITION_RANK.day,

finance.FUT_MEMBER_POSITION_RANK.code,

finance.FUT_MEMBER_POSITION_RANK.rank_type_ID,

finance.FUT_MEMBER_POSITION_RANK.rank,

finance.FUT_MEMBER_POSITION_RANK.member_name,

finance.FUT_MEMBER_POSITION_RANK.indicator,

finance.FUT_MEMBER_POSITION_RANK.indicator_increase,).filter(

finance.FUT_MEMBER_POSITION_RANK.code=='IC1906.CCFX',

finance.FUT_MEMBER_POSITION_RANK.rank_type_ID=='501003',

finance.FUT_MEMBER_POSITION_RANK.day==i).order_by(

finance.FUT_MEMBER_POSITION_RANK.member_name.desc())

df=finance.run_query(q)

for i in range(len(df)):

a = "中信期货"

if a in df.loc[i, 'member_name']:

a1 = df.loc[i, 'member_name']

a2 = df.loc[i, 'indicator']

a3 = df.loc[i, 'indicator_increase']

a4 = df.loc[i, 'code']

a5 = df.loc[i,'day']

c1.append(a1)

c2.append(a2)

c3.append(a3)

c4.append(a4)

c5.append(a5)

for i in range(len(df)):

a = "海通期货"

if a in df.loc[i, 'member_name']:

a1 = df.loc[i, 'member_name']

a2 = df.loc[i, 'indicator']

a3 = df.loc[i, 'indicator_increase']

a4 = df.loc[i, 'code']

a5 = df.loc[i, 'day']

c11.append(a1)

c12.append(a2)

c13.append(a3)

c14.append(a4)

c15.append(a5)

for i in range(len(df)):

a = "国泰君安"

if a in df.loc[i, 'member_name']:

a1 = df.loc[i, 'member_name']

a2 = df.loc[i, 'indicator']

a3 = df.loc[i, 'indicator_increase']

a4 = df.loc[i, 'code']

a5 = df.loc[i, 'day']

c21.append(a1)

c22.append(a2)

c23.append(a3)

c24.append(a4)

c25.append(a5)

for i in range(len(df)):

a = "华泰期货"

if a in df.loc[i, 'member_name']:

a1 = df.loc[i, 'member_name']

a2 = df.loc[i, 'indicator']

a3 = df.loc[i, 'indicator_increase']

a4 = df.loc[i, 'code']

a5 = df.loc[i, 'day']

c31.append(a1)

c32.append(a2)

c33.append(a3)

c34.append(a4)

c35.append(a5)

f2 = pd.DataFrame(columns=['day', 'member_name', 'indicator','indicator_increase'])

f2['day']=c5

f2[ 'member_name'] = c1

f2['indicator'] = c2

f2['indicator_increase']=c3

f2 = f2.set_index(['day'])

f12 = pd.DataFrame(columns=['day', 'member_name', 'indicator','indicator_increase'])

f12['day']=c15

f12[ 'member_name'] = c11

f12['indicator'] = c12

f12['indicator_increase']=c13

f12 = f12.set_index(['day'])

f22 = pd.DataFrame(columns=['day', 'member_name', 'indicator','indicator_increase'])

f22['day']=c25

f22[ 'member_name'] = c21

f22['indicator'] = c22

f22['indicator_increase']=c23

f22 = f22.set_index(['day'])

f32 = pd.DataFrame(columns=['day', 'member_name', 'indicator','indicator_increase'])

f32['day']=c35

f32[ 'member_name'] = c31

f32['indicator'] =c32

f32['indicator_increase']=c33

f32 = f32.set_index(['day'])

#501001-成交量排名

for k in date:

q=query(finance.FUT_MEMBER_POSITION_RANK.day,

finance.FUT_MEMBER_POSITION_RANK.code,

finance.FUT_MEMBER_POSITION_RANK.rank_type_ID,

finance.FUT_MEMBER_POSITION_RANK.rank,

finance.FUT_MEMBER_POSITION_RANK.member_name,

finance.FUT_MEMBER_POSITION_RANK.indicator,

finance.FUT_MEMBER_POSITION_RANK.indicator_increase,).filter(

finance.FUT_MEMBER_POSITION_RANK.code=='IC1906.CCFX',

finance.FUT_MEMBER_POSITION_RANK.rank_type_ID=='501001',

finance.FUT_MEMBER_POSITION_RANK.day==k).order_by(

finance.FUT_MEMBER_POSITION_RANK.member_name.desc())

df=finance.run_query(q)

for i in range(len(df)):

a = "中信期货"

if a in df.loc[i, 'member_name']:

a1 = df.loc[i, 'member_name']

a2 = df.loc[i, 'indicator']

a3 = df.loc[i, 'indicator_increase']

a4 = df.loc[i, 'code']

a5 = df.loc[i,'day']

d1.append(a1)

d2.append(a2)

d3.append(a3)

d4.append(a4)

d5.append(a5)

for i in range(len(df)):

a = "海通期货"

if a in df.loc[i, 'member_name']:

a1 = df.loc[i, 'member_name']

a2 = df.loc[i, 'indicator']

a3 = df.loc[i, 'indicator_increase']

a4 = df.loc[i, 'code']

a5 = df.loc[i, 'day']

d11.append(a1)

d12.append(a2)

d13.append(a3)

d14.append(a4)

d15.append(a5)

for i in range(len(df)):

a = "国泰君安"

if a in df.loc[i, 'member_name']:

a1 = df.loc[i, 'member_name']

a2 = df.loc[i, 'indicator']

a3 = df.loc[i, 'indicator_increase']

a4 = df.loc[i, 'code']

a5 = df.loc[i, 'day']

d21.append(a1)

d22.append(a2)

d23.append(a3)

d24.append(a4)

d25.append(a5)

for i in range(len(df)):

a = "华泰期货"

if a in df.loc[i, 'member_name']:

a1 = df.loc[i, 'member_name']

a2 = df.loc[i, 'indicator']

a3 = df.loc[i, 'indicator_increase']

a4 = df.loc[i, 'code']

a5 = df.loc[i, 'day']

d31.append(a1)

d32.append(a2)

d33.append(a3)

d34.append(a4)

d35.append(a5)

f3 = pd.DataFrame(columns=['day', 'member_name', 'indicator','indicator_increase'])

f3['day']=d5

f3[ 'member_name'] = d1

f3['indicator'] = d2

f3['indicator_increase']=d3

f3 = f3.set_index(['day'])

f13 = pd.DataFrame(columns=['day', 'member_name', 'indicator','indicator_increase'])

f13['day']=d15

f13[ 'member_name'] = d11

f13['indicator'] = d12

f13['indicator_increase']=d13

f13 = f13.set_index(['day'])

f23 = pd.DataFrame(columns=['day', 'member_name', 'indicator','indicator_increase'])

f23['day']=d25

f23[ 'member_name'] = d21

f23['indicator'] = d22

f23['indicator_increase']=d23

f23 = f23.set_index(['day'])

f33 = pd.DataFrame(columns=['day', 'member_name', 'indicator','indicator_increase'])

f33['day']=d35

f33[ 'member_name'] = d31

f33['indicator'] = d32

f33['indicator_increase']=d33

f33 = f33.set_index(['day'])

print(f2)

print(f12)

#1

N = len(f1)

ind = np.arange(N) # the evenly spaced plot indices

def format_date(x, pos=None):

#保证下标不越界,很重要,越界会导致最终plot坐标轴label无显示

thisind = np.clip(int(x+0.5), 0, N-1)

return f1.index[thisind].strftime('%Y-%m-%d')

N2 = len(f2)

ind2 = np.arange(N2) # the evenly spaced plot indices

N3 = len(f3)

ind3 = np.arange(N3) # the evenly spaced plot indices

#2

AN = len(f11)

Aind = np.arange(AN) # the evenly spaced plot indices

def Aformat_date(x, pos=None):

#保证下标不越界,很重要,越界会导致最终plot坐标轴label无显示

thisind = np.clip(int(x+0.5), 0, AN-1)

return f11.index[thisind].strftime('%Y-%m-%d')

AN2 = len(f12)

Aind2 = np.arange(AN2) # the evenly spaced plot indices

AN3 = len(f13)

Aind3 = np.arange(AN3) # the evenly spaced plot indices

#3

BN = len(f21)

Bind = np.arange(BN) # the evenly spaced plot indices

def Bformat_date(x, pos=None):

#保证下标不越界,很重要,越界会导致最终plot坐标轴label无显示

thisind = np.clip(int(x+0.5), 0, BN-1)

return f21.index[thisind].strftime('%Y-%m-%d')

BN2 = len(f22)

Bind2 = np.arange(BN2) # the evenly spaced plot indices

BN3 = len(f23)

Bind3 = np.arange(BN3) # the evenly spaced plot indices

#4

CN = len(f31)

Cind = np.arange(CN) # the evenly spaced plot indices

def Cformat_date(x, pos=None):

#保证下标不越界,很重要,越界会导致最终plot坐标轴label无显示

thisind = np.clip(int(x+0.5), 0, CN-1)

return f31.index[thisind].strftime('%Y-%m-%d')

CN2 = len(f32)

Cind2 = np.arange(CN2) # the evenly spaced plot indices

CN3 = len(f33)

Cind3 = np.arange(CN3) # the evenly spaced plot indices

fig = plt.figure(figsize=(15,10))

#1

ax1 = fig.add_subplot(2,2,1)

ax1.plot(ind,f1.indicator, color="red",label="持买单量", marker='.',alpha=0.8, linewidth=0.6)

ax1.set_title("IC1905 中信期货持仓情况")

for j in range(1, len(f1)):

plt.text(ind[j],f1.indicator[j], str(f1.indicator[j]), fontsize=10, va='bottom', color="red", wrap=True)

ax1.plot(ind2,f2.indicator, color="green",label="持卖单量", marker='.', alpha=0.8, linewidth=0.6)

for j in range(1, len(f2)):

plt.text(ind2[j],f2.indicator[j], str(f2.indicator[j]), fontsize=10, ha='right', color="green", wrap=True)

ax1.plot(ind3,f3.indicator, color="blue",label="当日成交量", marker='.', alpha=0.8, linewidth=0.6)

for j in range(1, len(f3)):

plt.text(ind3[j],f3.indicator[j], str(f3.indicator[j]), fontsize=10, ha='left', color="blue", wrap=True)

#2

bx1 = fig.add_subplot(2,2,2)

bx1.plot(Aind,f11.indicator, color="red",label="持买单量", marker='.',alpha=0.8, linewidth=0.6)

bx1.set_title("IC1905 海通期货持仓情况")

for j in range(1, len(f11)):

plt.text(Aind[j],f11.indicator[j], str(f11.indicator[j]), fontsize=10, va='bottom', color="red", wrap=True)

bx1.plot(Aind2,f12.indicator, color="green",label="持卖单量", marker='.',alpha=0.8, linewidth=0.6)

for j in range(1, len(f12)):

plt.text(Aind2[j],f12.indicator[j], str(f12.indicator[j]), fontsize=10, ha='right', color="green", wrap=True)

bx1.plot(Aind3,f13.indicator, color="blue",label="当日成交量",marker='.', alpha=0.8, linewidth=0.6)

for j in range(1, len(f13)):

plt.text(Aind3[j],f13.indicator[j], str(f13.indicator[j]), fontsize=10, ha='left', color="blue", wrap=True)

#3

cx1 = fig.add_subplot(2,2,3)

cx1.plot(Bind,f21.indicator, color="red",label="持买单量", marker='.',alpha=0.8, linewidth=0.6)

cx1.set_title("IC1905 国泰君安持仓情况")

for j in range(1, len(f21)):

plt.text(Bind[j],f21.indicator[j], str(f21.indicator[j]), fontsize=10, va='bottom', color="red", wrap=True)

cx1.plot(Bind2,f22.indicator, color="green",label="持卖单量",marker='.', alpha=0.8, linewidth=0.6)

for j in range(1, len(f22)):

plt.text(Bind2[j],f22.indicator[j], str(f22.indicator[j]), fontsize=10, ha='right', color="green", wrap=True)

cx1.plot(Bind3,f23.indicator, color="blue",label="当日成交量",marker='.', alpha=0.8, linewidth=0.6)

for j in range(1, len(f23)):

plt.text(Bind3[j],f23.indicator[j], str(f23.indicator[j]), fontsize=10, ha='left', color="blue", wrap=True)

#4

dx1 = fig.add_subplot(2,2,4)

dx1.plot(Cind,f31.indicator, color="red",label="持买单量", marker='.',alpha=0.8, linewidth=0.6)

dx1.set_title("IC1905 华泰期货持仓情况")

for j in range(1, len(f31)):

plt.text(Cind[j],f31.indicator[j], str(f31.indicator[j]), fontsize=10, va='bottom', color="red", wrap=True)

dx1.plot(Cind2,f32.indicator, color="green",label="持卖单量", marker='.',alpha=0.8, linewidth=0.6)

for j in range(1, len(f32)):

plt.text(Cind2[j],f32.indicator[j], str(f32.indicator[j]), fontsize=10, ha='right', color="green", wrap=True)

dx1.plot(Cind3,f33.indicator, color="blue",label="当日成交量",marker='.', alpha=0.8, linewidth=0.6)

for j in range(1, len(f33)):

plt.text(Cind3[j],f33.indicator[j], str(f33.indicator[j]), fontsize=10, ha='left', color="blue", wrap=True)

ax1.xaxis.set_major_formatter(ticker.FuncFormatter(format_date))

bx1.xaxis.set_major_formatter(ticker.FuncFormatter(Aformat_date))

cx1.xaxis.set_major_formatter(ticker.FuncFormatter(Bformat_date))

dx1.xaxis.set_major_formatter(ticker.FuncFormatter(Cformat_date))

fig.autofmt_xdate()

handles, labels = ax1.get_legend_handles_labels()

# reverse the order

ax1.legend(handles[::-1], labels[::-1])

handles, labels = bx1.get_legend_handles_labels()

# reverse the order

bx1.legend(handles[::-1], labels[::-1])

handles, labels = cx1.get_legend_handles_labels()

# reverse the order

cx1.legend(handles[::-1], labels[::-1])

handles, labels = dx1.get_legend_handles_labels()

# reverse the order

dx1.legend(handles[::-1], labels[::-1])

plt.savefig('IC1905.png')

plt.show()

r=pd.concat([price.close,

f1.indicator,

f2.indicator,

f3.indicator,

f11.indicator,

f12.indicator,

f13.indicator,

f21.indicator,

f22.indicator,

f23.indicator,

f31.indicator,

f32.indicator,

f33.indicator],axis=1)

r.columns = ['pct', 'citic_long','citic_short','citic_change',

'ht_long','ht_short','ht_change',

'gtja_long','gtja_short','gtja_change',

'ht_long','ht_short','ht_change']

r.to_csv('future_re.csv')

#2画图

import plotly.plotly as py

import plotly.graph_objs as go

import plotly

import plotly.graph_objs as go

import numpy as np

import pandas as pd

from jqdatasdk import *

auth('','')

import pandas as pd

import talib

df = pd.read_csv('future_re.csv')

future_jq= get_price('IF1906.CCFX', end_date='2019-05-17',count=50)

# remove min:sec:millisec from dates

'''for i, row in enumerate(df['Date']):

p = re.compile(' 00:00:00')

datetime = p.split(df['Date'][i])[0]

df.iloc[i, 1] = datetime'''

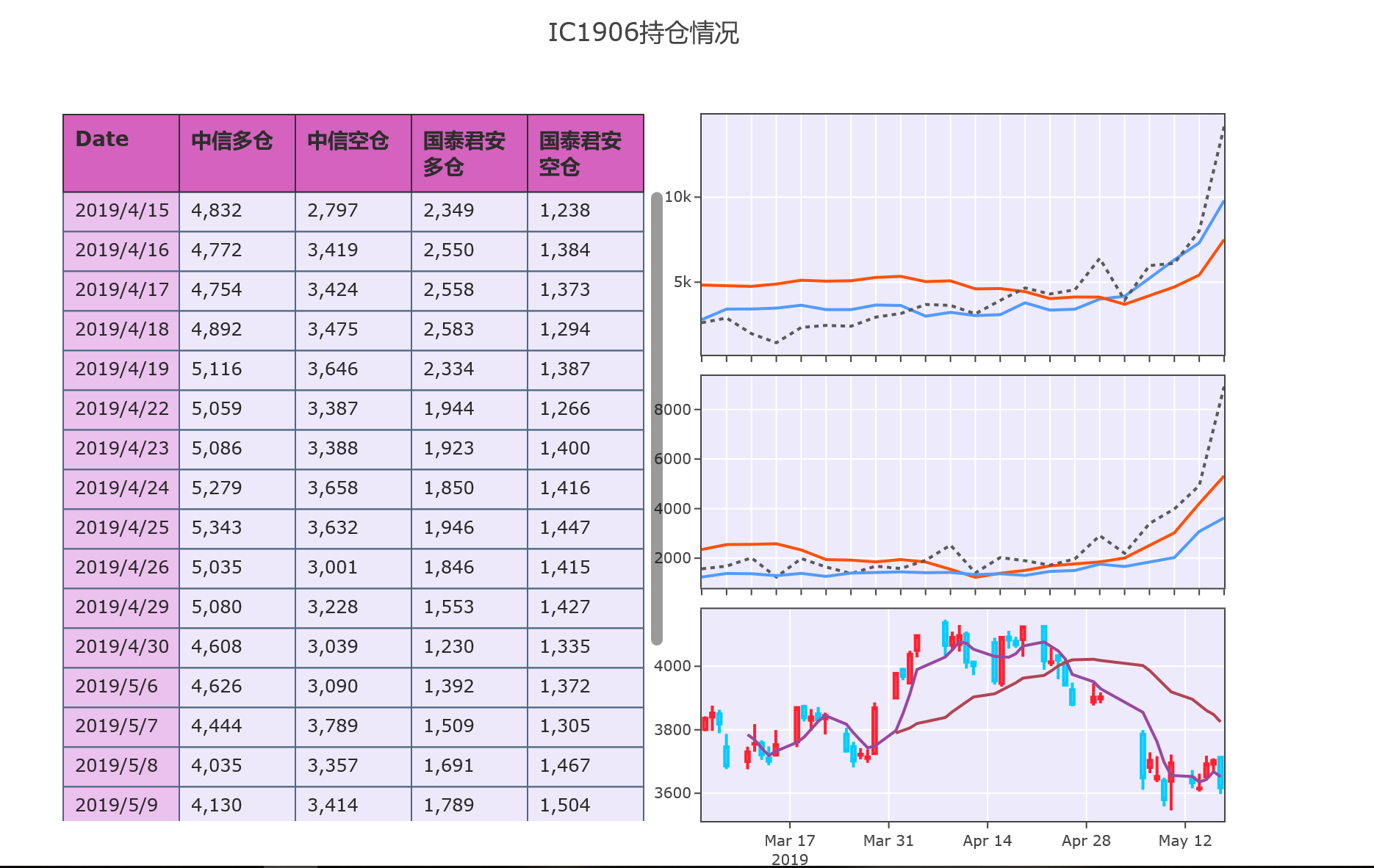

table_trace1 = go.Table(

domain=dict(x=[0, 0.5],

y=[0, 1]),

columnwidth = [20] + [20, 20, 20,20],

columnorder=[0, 1, 2, 3, 4,5],

header = dict(height = 50,

values = [['<b>Date</b>'],['<b>中信多仓</b>'],

['<b>中信空仓</b>'], ['<b>国泰君安<br>多仓</b>'],['<b>国泰君安<br>空仓</b>']],

line = dict(color='rgb(50, 50, 50)'),

align = ['left'] * 5,

font = dict(color=['rgb(45, 45, 45)'] * 6, size=14),

fill = dict(color='#d562be')),

cells = dict(values = [df[k].tolist() for k in

['date', 'citic_long', 'citic_short', 'gtja_long','gtja_short']],

line = dict(color='#506784'),

align = ['left'] * 6,

font = dict(color=['rgb(40, 40, 40)'] * 6, size=12),

format = [None] + [", .2f"] *4 ,

prefix = [None] * 5 ,

suffix=[None] * 5,

height = 27,

fill = dict(color=['rgb(235, 193, 238)', 'rgba(228, 222, 249, 0.65)']))

)

trace1 =go.Scatter(

x=df['date'],

y=df['citic_short'],

xaxis='x1',

yaxis='y1',

mode='lines',

line=dict(width=2, color='#509BFF'),

name='中信空仓'

)

trace11=go.Scatter(

x=df['date'],

y=df['citic_long'],

xaxis='x1',

yaxis='y1',

mode='lines',

line=dict(width=2, color='#FF5108'),

name='中信多仓'

)

trace12=go.Scatter(

x=df['date'],

y=df['citic_change'],

xaxis='x1',

yaxis='y1',

mode='lines',

line=dict(width=2, dash = 'dot',color='#595959'),

name='中信换手'

)

trace2=go.Scatter(

x=df['date'],

y=df['gtja_long'],

xaxis='x2',

yaxis='y2',

mode='lines',

line=dict(width=2, color='#FF5108'),

name='国泰君安空仓'

)

trace21 =go.Scatter(

x=df['date'],

y=df['gtja_change'],

xaxis='x2',

yaxis='y2',

mode='lines',

line=dict(width=2,dash = 'dot', color='#595959'),

name='国泰君安换手'

)

trace22 =go.Scatter(

x=df['date'],

y=df['gtja_short'],

xaxis='x2',

yaxis='y2',

mode='lines',

line=dict(width=2, color='#509BFF'),

name='国泰君安多仓'

)

trace3 = go.Candlestick(x=future_jq.index,

xaxis='x3',

yaxis='y3',

open=future_jq.open,

high=future_jq.high,

low=future_jq.low,

close=future_jq.close,

name = "IC1906",

increasing=dict(line=dict(color='#FF2131')),

decreasing=dict(line=dict(color='#00CCFF'))

)

trace31 =go.Scatter(

x=future_jq.index,

y=talib.MA(future_jq.close,5),

xaxis='x3',

yaxis='y3',

mode='lines',

line=dict(width=2, color='#9748a1'),

name='MA5'

)

trace32 =go.Scatter(

x=future_jq.index,

y=talib.MA(future_jq.close,20),

xaxis='x3',

yaxis='y3',

mode='lines',

line=dict(width=2, color='#b04553'),

name='MA20'

)

axis=dict(

showline=True,

zeroline=False,

showgrid=True,

mirror=True,

ticklen=4,

gridcolor='#ffffff',

tickfont=dict(size=10)

)

layout1 = dict(

width=950,

height=800,

autosize=False,

title='IC1906持仓情况',

margin = dict(t=100),

showlegend=False,

xaxis1=dict(axis, **dict(domain=[0.55, 1], anchor='y1', showticklabels=False)),

xaxis2=dict(axis, **dict(domain=[0.55, 1], anchor='y2', showticklabels=False)),

xaxis3=dict(axis, **dict(domain=[0.55, 1], anchor='y3')),

yaxis1=dict(axis, **dict(domain=[0.66, 1.0], anchor='x1')),

yaxis2=dict(axis, **dict(domain=[0.3 + 0.03, 0.63], anchor='x2')),

yaxis3=dict(axis, **dict(domain=[0.0, 0.3], anchor='x3')),

plot_bgcolor='rgba(228, 222, 249, 0.65)'

)

#tickprefix='$',

fig1 = dict(data=[table_trace1, trace1,trace11,trace12,trace2,trace21,trace22, trace3,trace31,trace32 ], layout=layout1)

plotly.offline.plot(fig1, filename='table.html')

本社区仅针对特定人员开放

查看需注册登录并通过风险意识测评

5秒后跳转登录页面...

移动端课程