市场风格变化莫测,交易中总是抓不住市场的节奏,而且我等韭菜也疲于日常工作,迫于资源限制,投资股市时不能做到既关注实时热点,把握大势,又了解行业,深究公司,这样一来,似乎已经落后那些花大力气在做行业研究,公司研究的机构或者大牛们。然而,也不尽然如此,毕竟,对股市所有的看法,最终落地都是参与市场进行交易,总是在市场上留下痕迹。研究量价特征,不失为一种讨巧的办法。

以上就是技术分析爱好者的理论基础了,这对于众多没有便利的渠道掌握一手信息,没有丰富的知识储备分析大势的散户来说,是个好消息,在这个层面来讲,大家几乎掌握着一致的信息,问题就在于谁能挖掘出更多的价值信息。同样,这最轻松的投资方式,也可能是因为这种方式投资成本最低,画几条趋势线,认几个形态,就能做出买卖决定,从市场中赚钱,这可能就是交易吸引人的地方了,也是交易不容易赚钱的原因了,哈哈哈,扯远了都。

下面的内容就是想研究市场的量价方面的特征,因子来源于国泰君安数量化专题,内容参考短周期价量特征的多因子选股体系的内容,在聚宽上尝试建立因子效果检查部分内容,也参考了之前止一之路的帖子。

因子数据计算时因为有点耗时,本篇文章中只用到了alpha191因子的第一个因子数据进行了演示说明,将因子值计算出来,行业市值中性,计算不同周期长度的收益,后面若有兴趣可以进行类似的尝试计算更多的结果。

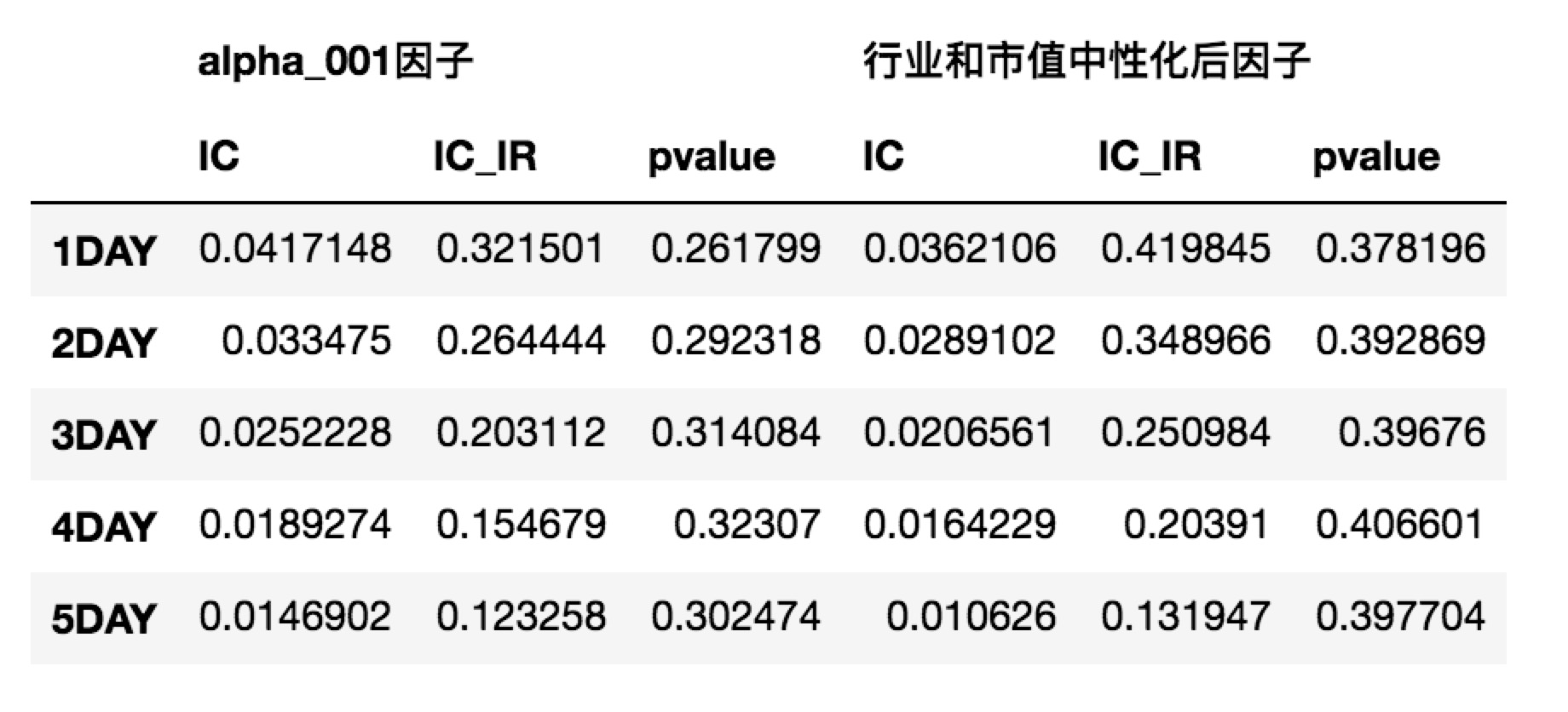

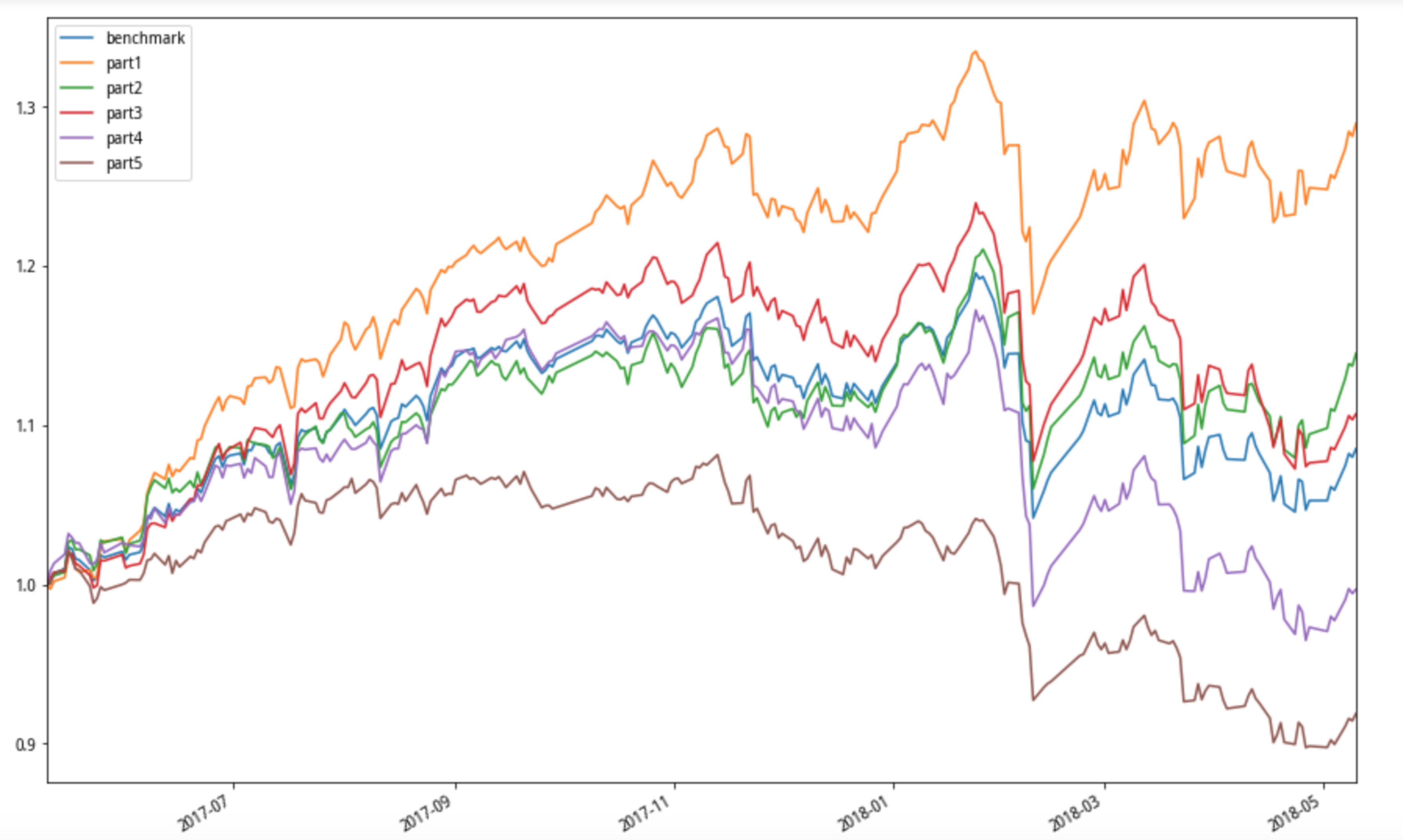

貌似中性化处理后,并没有太过明显的差距,后面可以考虑剔除更多的风格因子,关于代码或者处理方法都可以留言一起探讨

import pandas as pd

import numpy as np

from jqlib.alpha191 import *

import jqdata

import datetime

import time

import statsmodels.api as sm

import scipy.stats as st

import math

from statsmodels import regression

import matplotlib.pyplot as plt

/opt/conda/envs/python2new/lib/python2.7/site-packages/statsmodels/compat/pandas.py:56: FutureWarning: The pandas.core.datetools module is deprecated and will be removed in a future version. Please use the pandas.tseries module instead. from pandas.core import datetools

#计算并保存alpha002因子值

#参数:开始时间,结束时间,股票池,不同alpha因子的API

#输出:index为日期,column是股票名称,values是因子值的dataframe

#将alpha因子值保存为CSV格式文件,使用时直接调用

df_sh50 = get_price('000300.XSHG',start_date='2017-5-10',end_date='2018-5-10')

index_date = df_sh50.index

#对于不同时期的成分股不一致的情况,经过检查,对对columns进行校验

columns_stock = get_index_stocks('000300.XSHG')

alpha_002_factor = pd.DataFrame(index = index_date,columns = columns_stock)

alpha_002_factor_neu = pd.DataFrame(index = index_date,columns = columns_stock)

for i in index_date:

print i

code= list(get_index_stocks('000300.XSHG'))

temp_a = alpha_002(code,i)

#temp_a_neu = get_factor_ne(temp_a,i)['factor_ne']

temp_a = temp_a.dropna()

temp_a_neu = get_factor_neutra(temp_a,i)

#print temp_a_neu

alpha_002_factor.loc[i,:] = temp_a

#中性化后的因子值

alpha_002_factor_neu.loc[i,:] = temp_a_neu

alpha_002_factor.to_csv('alpha_002.csv')

alpha_002_factor_neu.to_csv('alpha_002_neutra.csv')

2017-05-10 00:00:00 2017-05-11 00:00:00 2017-05-12 00:00:00 2017-05-15 00:00:00 2017-05-16 00:00:00 2017-05-17 00:00:00 2017-05-18 00:00:00 2017-05-19 00:00:00 2017-05-22 00:00:00 2017-05-23 00:00:00 2017-05-24 00:00:00 2017-05-25 00:00:00 2017-05-26 00:00:00 2017-05-31 00:00:00 2017-06-01 00:00:00 2017-06-02 00:00:00 2017-06-05 00:00:00 2017-06-06 00:00:00 2017-06-07 00:00:00 2017-06-08 00:00:00 2017-06-09 00:00:00 2017-06-12 00:00:00 2017-06-13 00:00:00 2017-06-14 00:00:00 2017-06-15 00:00:00 2017-06-16 00:00:00 2017-06-19 00:00:00 2017-06-20 00:00:00 2017-06-21 00:00:00 2017-06-22 00:00:00 2017-06-23 00:00:00 2017-06-26 00:00:00 2017-06-27 00:00:00 2017-06-28 00:00:00 2017-06-29 00:00:00 2017-06-30 00:00:00 2017-07-03 00:00:00 2017-07-04 00:00:00 2017-07-05 00:00:00 2017-07-06 00:00:00 2017-07-07 00:00:00 2017-07-10 00:00:00 2017-07-11 00:00:00 2017-07-12 00:00:00 2017-07-13 00:00:00 2017-07-14 00:00:00 2017-07-17 00:00:00 2017-07-18 00:00:00 2017-07-19 00:00:00 2017-07-20 00:00:00 2017-07-21 00:00:00 2017-07-24 00:00:00 2017-07-25 00:00:00 2017-07-26 00:00:00 2017-07-27 00:00:00 2017-07-28 00:00:00 2017-07-31 00:00:00 2017-08-01 00:00:00 2017-08-02 00:00:00 2017-08-03 00:00:00 2017-08-04 00:00:00 2017-08-07 00:00:00 2017-08-08 00:00:00 2017-08-09 00:00:00 2017-08-10 00:00:00 2017-08-11 00:00:00 2017-08-14 00:00:00 2017-08-15 00:00:00 2017-08-16 00:00:00 2017-08-17 00:00:00 2017-08-18 00:00:00 2017-08-21 00:00:00 2017-08-22 00:00:00 2017-08-23 00:00:00 2017-08-24 00:00:00 2017-08-25 00:00:00 2017-08-28 00:00:00 2017-08-29 00:00:00 2017-08-30 00:00:00 2017-08-31 00:00:00 2017-09-01 00:00:00 2017-09-04 00:00:00 2017-09-05 00:00:00 2017-09-06 00:00:00 2017-09-07 00:00:00 2017-09-08 00:00:00 2017-09-11 00:00:00 2017-09-12 00:00:00 2017-09-13 00:00:00 2017-09-14 00:00:00 2017-09-15 00:00:00 2017-09-18 00:00:00 2017-09-19 00:00:00 2017-09-20 00:00:00 2017-09-21 00:00:00 2017-09-22 00:00:00 2017-09-25 00:00:00 2017-09-26 00:00:00 2017-09-27 00:00:00 2017-09-28 00:00:00 2017-09-29 00:00:00 2017-10-09 00:00:00 2017-10-10 00:00:00 2017-10-11 00:00:00 2017-10-12 00:00:00 2017-10-13 00:00:00 2017-10-16 00:00:00 2017-10-17 00:00:00 2017-10-18 00:00:00 2017-10-19 00:00:00 2017-10-20 00:00:00 2017-10-23 00:00:00 2017-10-24 00:00:00 2017-10-25 00:00:00 2017-10-26 00:00:00 2017-10-27 00:00:00 2017-10-30 00:00:00 2017-10-31 00:00:00 2017-11-01 00:00:00 2017-11-02 00:00:00 2017-11-03 00:00:00 2017-11-06 00:00:00 2017-11-07 00:00:00 2017-11-08 00:00:00 2017-11-09 00:00:00 2017-11-10 00:00:00 2017-11-13 00:00:00 2017-11-14 00:00:00 2017-11-15 00:00:00 2017-11-16 00:00:00 2017-11-17 00:00:00 2017-11-20 00:00:00 2017-11-21 00:00:00 2017-11-22 00:00:00 2017-11-23 00:00:00 2017-11-24 00:00:00 2017-11-27 00:00:00 2017-11-28 00:00:00 2017-11-29 00:00:00 2017-11-30 00:00:00 2017-12-01 00:00:00 2017-12-04 00:00:00 2017-12-05 00:00:00 2017-12-06 00:00:00 2017-12-07 00:00:00 2017-12-08 00:00:00 2017-12-11 00:00:00 2017-12-12 00:00:00 2017-12-13 00:00:00 2017-12-14 00:00:00 2017-12-15 00:00:00 2017-12-18 00:00:00 2017-12-19 00:00:00 2017-12-20 00:00:00 2017-12-21 00:00:00 2017-12-22 00:00:00 2017-12-25 00:00:00 2017-12-26 00:00:00 2017-12-27 00:00:00 2017-12-28 00:00:00 2017-12-29 00:00:00 2018-01-02 00:00:00 2018-01-03 00:00:00 2018-01-04 00:00:00 2018-01-05 00:00:00 2018-01-08 00:00:00 2018-01-09 00:00:00 2018-01-10 00:00:00 2018-01-11 00:00:00 2018-01-12 00:00:00 2018-01-15 00:00:00 2018-01-16 00:00:00 2018-01-17 00:00:00 2018-01-18 00:00:00 2018-01-19 00:00:00 2018-01-22 00:00:00 2018-01-23 00:00:00 2018-01-24 00:00:00 2018-01-25 00:00:00 2018-01-26 00:00:00 2018-01-29 00:00:00 2018-01-30 00:00:00 2018-01-31 00:00:00 2018-02-01 00:00:00 2018-02-02 00:00:00 2018-02-05 00:00:00 2018-02-06 00:00:00 2018-02-07 00:00:00 2018-02-08 00:00:00 2018-02-09 00:00:00 2018-02-12 00:00:00 2018-02-13 00:00:00 2018-02-14 00:00:00 2018-02-22 00:00:00 2018-02-23 00:00:00 2018-02-26 00:00:00 2018-02-27 00:00:00 2018-02-28 00:00:00 2018-03-01 00:00:00 2018-03-02 00:00:00 2018-03-05 00:00:00 2018-03-06 00:00:00 2018-03-07 00:00:00 2018-03-08 00:00:00 2018-03-09 00:00:00 2018-03-12 00:00:00 2018-03-13 00:00:00 2018-03-14 00:00:00 2018-03-15 00:00:00 2018-03-16 00:00:00 2018-03-19 00:00:00 2018-03-20 00:00:00 2018-03-21 00:00:00 2018-03-22 00:00:00 2018-03-23 00:00:00 2018-03-26 00:00:00 2018-03-27 00:00:00 2018-03-28 00:00:00 2018-03-29 00:00:00 2018-03-30 00:00:00 2018-04-02 00:00:00 2018-04-03 00:00:00 2018-04-04 00:00:00 2018-04-09 00:00:00 2018-04-10 00:00:00 2018-04-11 00:00:00 2018-04-12 00:00:00 2018-04-13 00:00:00 2018-04-16 00:00:00 2018-04-17 00:00:00 2018-04-18 00:00:00 2018-04-19 00:00:00 2018-04-20 00:00:00 2018-04-23 00:00:00 2018-04-24 00:00:00 2018-04-25 00:00:00 2018-04-26 00:00:00 2018-04-27 00:00:00 2018-05-02 00:00:00 2018-05-03 00:00:00 2018-05-04 00:00:00 2018-05-07 00:00:00 2018-05-08 00:00:00 2018-05-09 00:00:00 2018-05-10 00:00:00

#计算并保存alpha003因子值

#参数:开始时间,结束时间,股票池,不同alpha因子的API

#输出:index为日期,column是股票名称,values是因子值的dataframe

#将alpha因子值保存为CSV格式文件,使用时直接调用

df_sh50 = get_price('000300.XSHG',start_date='2017-5-10',end_date='2018-5-10')

index_date = df_sh50.index

#对于不同时期的成分股不一致的情况,经过检查,对对columns进行校验

columns_stock = get_index_stocks('000300.XSHG')

alpha_003_factor = pd.DataFrame(index = index_date,columns = columns_stock)

alpha_003_factor_neu = pd.DataFrame(index = index_date,columns = columns_stock)

for i in index_date:

print i

code= list(get_index_stocks('000300.XSHG'))

temp_a = alpha_003(code,i)

#temp_a_neu = get_factor_ne(temp_a,i)['factor_ne']

temp_a = temp_a.dropna()

temp_a_neu = get_factor_neutra(temp_a,i)

#print temp_a_neu

alpha_003_factor.loc[i,:] = temp_a

#中性化后的因子值

alpha_003_factor_neu.loc[i,:] = temp_a_neu

alpha_003_factor.to_csv('alpha_003.csv')

alpha_003_factor_neu.to_csv('alpha_003_neutra.csv')

2017-05-10 00:00:00 2017-05-11 00:00:00 2017-05-12 00:00:00 2017-05-15 00:00:00 2017-05-16 00:00:00 2017-05-17 00:00:00 2017-05-18 00:00:00 2017-05-19 00:00:00 2017-05-22 00:00:00 2017-05-23 00:00:00 2017-05-24 00:00:00 2017-05-25 00:00:00 2017-05-26 00:00:00 2017-05-31 00:00:00 2017-06-01 00:00:00 2017-06-02 00:00:00 2017-06-05 00:00:00 2017-06-06 00:00:00 2017-06-07 00:00:00 2017-06-08 00:00:00 2017-06-09 00:00:00 2017-06-12 00:00:00 2017-06-13 00:00:00 2017-06-14 00:00:00 2017-06-15 00:00:00 2017-06-16 00:00:00 2017-06-19 00:00:00 2017-06-20 00:00:00 2017-06-21 00:00:00 2017-06-22 00:00:00 2017-06-23 00:00:00 2017-06-26 00:00:00 2017-06-27 00:00:00 2017-06-28 00:00:00 2017-06-29 00:00:00 2017-06-30 00:00:00 2017-07-03 00:00:00 2017-07-04 00:00:00 2017-07-05 00:00:00 2017-07-06 00:00:00 2017-07-07 00:00:00 2017-07-10 00:00:00 2017-07-11 00:00:00 2017-07-12 00:00:00 2017-07-13 00:00:00 2017-07-14 00:00:00 2017-07-17 00:00:00 2017-07-18 00:00:00 2017-07-19 00:00:00 2017-07-20 00:00:00 2017-07-21 00:00:00 2017-07-24 00:00:00 2017-07-25 00:00:00 2017-07-26 00:00:00 2017-07-27 00:00:00 2017-07-28 00:00:00 2017-07-31 00:00:00 2017-08-01 00:00:00 2017-08-02 00:00:00 2017-08-03 00:00:00 2017-08-04 00:00:00 2017-08-07 00:00:00 2017-08-08 00:00:00 2017-08-09 00:00:00 2017-08-10 00:00:00 2017-08-11 00:00:00 2017-08-14 00:00:00 2017-08-15 00:00:00 2017-08-16 00:00:00 2017-08-17 00:00:00 2017-08-18 00:00:00 2017-08-21 00:00:00 2017-08-22 00:00:00 2017-08-23 00:00:00 2017-08-24 00:00:00 2017-08-25 00:00:00 2017-08-28 00:00:00 2017-08-29 00:00:00 2017-08-30 00:00:00 2017-08-31 00:00:00 2017-09-01 00:00:00 2017-09-04 00:00:00 2017-09-05 00:00:00 2017-09-06 00:00:00 2017-09-07 00:00:00 2017-09-08 00:00:00 2017-09-11 00:00:00 2017-09-12 00:00:00 2017-09-13 00:00:00 2017-09-14 00:00:00 2017-09-15 00:00:00 2017-09-18 00:00:00 2017-09-19 00:00:00 2017-09-20 00:00:00 2017-09-21 00:00:00 2017-09-22 00:00:00 2017-09-25 00:00:00 2017-09-26 00:00:00 2017-09-27 00:00:00 2017-09-28 00:00:00 2017-09-29 00:00:00 2017-10-09 00:00:00 2017-10-10 00:00:00 2017-10-11 00:00:00 2017-10-12 00:00:00 2017-10-13 00:00:00 2017-10-16 00:00:00 2017-10-17 00:00:00 2017-10-18 00:00:00 2017-10-19 00:00:00 2017-10-20 00:00:00 2017-10-23 00:00:00 2017-10-24 00:00:00 2017-10-25 00:00:00 2017-10-26 00:00:00 2017-10-27 00:00:00 2017-10-30 00:00:00 2017-10-31 00:00:00 2017-11-01 00:00:00 2017-11-02 00:00:00 2017-11-03 00:00:00 2017-11-06 00:00:00 2017-11-07 00:00:00 2017-11-08 00:00:00 2017-11-09 00:00:00 2017-11-10 00:00:00 2017-11-13 00:00:00 2017-11-14 00:00:00 2017-11-15 00:00:00 2017-11-16 00:00:00 2017-11-17 00:00:00 2017-11-20 00:00:00 2017-11-21 00:00:00 2017-11-22 00:00:00 2017-11-23 00:00:00 2017-11-24 00:00:00 2017-11-27 00:00:00 2017-11-28 00:00:00 2017-11-29 00:00:00 2017-11-30 00:00:00 2017-12-01 00:00:00 2017-12-04 00:00:00 2017-12-05 00:00:00 2017-12-06 00:00:00 2017-12-07 00:00:00 2017-12-08 00:00:00 2017-12-11 00:00:00 2017-12-12 00:00:00 2017-12-13 00:00:00 2017-12-14 00:00:00 2017-12-15 00:00:00 2017-12-18 00:00:00 2017-12-19 00:00:00 2017-12-20 00:00:00 2017-12-21 00:00:00 2017-12-22 00:00:00 2017-12-25 00:00:00 2017-12-26 00:00:00 2017-12-27 00:00:00 2017-12-28 00:00:00 2017-12-29 00:00:00 2018-01-02 00:00:00 2018-01-03 00:00:00 2018-01-04 00:00:00 2018-01-05 00:00:00 2018-01-08 00:00:00 2018-01-09 00:00:00 2018-01-10 00:00:00 2018-01-11 00:00:00 2018-01-12 00:00:00 2018-01-15 00:00:00 2018-01-16 00:00:00 2018-01-17 00:00:00 2018-01-18 00:00:00 2018-01-19 00:00:00 2018-01-22 00:00:00 2018-01-23 00:00:00 2018-01-24 00:00:00 2018-01-25 00:00:00 2018-01-26 00:00:00 2018-01-29 00:00:00 2018-01-30 00:00:00 2018-01-31 00:00:00 2018-02-01 00:00:00 2018-02-02 00:00:00 2018-02-05 00:00:00 2018-02-06 00:00:00 2018-02-07 00:00:00 2018-02-08 00:00:00 2018-02-09 00:00:00 2018-02-12 00:00:00 2018-02-13 00:00:00 2018-02-14 00:00:00 2018-02-22 00:00:00 2018-02-23 00:00:00 2018-02-26 00:00:00 2018-02-27 00:00:00 2018-02-28 00:00:00 2018-03-01 00:00:00 2018-03-02 00:00:00 2018-03-05 00:00:00 2018-03-06 00:00:00 2018-03-07 00:00:00 2018-03-08 00:00:00 2018-03-09 00:00:00 2018-03-12 00:00:00 2018-03-13 00:00:00 2018-03-14 00:00:00 2018-03-15 00:00:00 2018-03-16 00:00:00 2018-03-19 00:00:00 2018-03-20 00:00:00 2018-03-21 00:00:00 2018-03-22 00:00:00 2018-03-23 00:00:00 2018-03-26 00:00:00 2018-03-27 00:00:00 2018-03-28 00:00:00 2018-03-29 00:00:00 2018-03-30 00:00:00 2018-04-02 00:00:00 2018-04-03 00:00:00 2018-04-04 00:00:00 2018-04-09 00:00:00 2018-04-10 00:00:00 2018-04-11 00:00:00 2018-04-12 00:00:00 2018-04-13 00:00:00 2018-04-16 00:00:00 2018-04-17 00:00:00 2018-04-18 00:00:00 2018-04-19 00:00:00 2018-04-20 00:00:00 2018-04-23 00:00:00 2018-04-24 00:00:00 2018-04-25 00:00:00 2018-04-26 00:00:00 2018-04-27 00:00:00 2018-05-02 00:00:00 2018-05-03 00:00:00 2018-05-04 00:00:00 2018-05-07 00:00:00 2018-05-08 00:00:00 2018-05-09 00:00:00 2018-05-10 00:00:00

#中性化(回归拟合后取残差值为因子的最新值)

#传入:mkt_cap:以股票为index,市值为value的Series,

#factor:以股票code为index,因子值为value的Series,

#输出:中性化后的因子值series

def neutralization(factor,mkt_cap = False, industry = True,date=None):

y = factor

if type(mkt_cap) == pd.Series:

LnMktCap = mkt_cap.apply(lambda x:math.log(x))

if industry: #行业、市值

dummy_industry = get_industry_exposure(factor.index,date)

x = pd.concat([LnMktCap,dummy_industry.T],axis = 1)

else: #仅市值

x = LnMktCap

elif industry: #仅行业

dummy_industry = get_industry_exposure(factor.index)

x = dummy_industry.T

result = sm.OLS(y.astype(float),x.astype(float)).fit()

return result.resid

#为股票池添加行业标记,return df格式 ,为中性化函数的子函数

def get_industry_exposure(stock_list,date):

df = pd.DataFrame(index=jqdata.get_industries(name='sw_l1').index, columns=stock_list)

for stock in stock_list:

try:

df[stock][get_industry_code_from_security(stock,date)] = 1

except:

continue

return df.fillna(0)#将NaN赋为0

#查询个股所在行业函数代码(申万一级) ,为中性化函数的子函数

def get_industry_code_from_security(security,date=None):

industry_index=jqdata.get_industries(name='sw_l1').index

for i in range(0,len(industry_index)):

try:

index = get_industry_stocks(industry_index[i],date=date).index(security)

return industry_index[i]

except:

continue

return u'未找到'

def get_factor_neutra(alpha_factor,date):

h=get_fundamentals(query(valuation.code,valuation.market_cap)\

.filter(valuation.code.in_(alpha_factor.index)),date=date)

stocks_mktcap_se=pd.Series(list(h.market_cap),index=list(h.code))

stocks_neutra_se=neutralization(alpha_factor,stocks_mktcap_se,date)

return stocks_neutra_se

#按行业进行标准化处理的方法

#参数:

#输入:股票名称为index的因子序列,检查日期

#输出: df,包括市值,包括因子值

def get_factor_ne(factor_se,date):

industries = jqdata.get_industries(name='sw_l1').index

df_factor = get_fundamentals(query(valuation.code,valuation.market_cap).filter(valuation.code.in_(factor_se.index)),date)

df_factor.index = df_factor.code

del df_factor['code']

df_factor.columns = ['market_cap']

df_factor['factor'] = factor_se

industries_series = pd.Series()

for aa in industries:

alist = []

stock_list = list(get_industry_stocks(aa, date=date))

for bb in stock_list:

if bb in list(df_factor.index):

alist.append(bb)

aseries = pd.Series(aa, index = alist)

# print aseries

industries_series = pd.concat([industries_series, aseries])

duplicated = industries_series.index.duplicated()

index_list = []

for x in range(len(industries_series.index)):

if duplicated[x] ==True:

index_list.append(list(industries_series.index)[x])

industries_series.drop(index_list, inplace = True)

df_factor['industries_detail'] = industries_series

df_factor.dropna(how = 'any', inplace = True) # 1173/1018 2016/12/31

df_factor['factor_mean'] = NaN

df_factor['factor_std'] = NaN

for x in range(len(industries)):

# 生成均值数据

df_factor['factor_mean'][df_factor['industries_detail'] == industries[x]] \

= df_factor['factor'][df_factor['industries_detail'] == industries[x]].mean()

# 生成方差数据

df_factor['factor_std'][df_factor['industries_detail'] == industries[x]] \

= df_factor['factor'][df_factor['industries_detail'] == industries[x]].std()

# 标准化

df_factor['factor_ne'] = (df_factor['factor'] - df_factor['factor_mean'])/df_factor['factor_std']

#df_factor.dropna(how = 'any', inplace = True)

return df_factor

#进行收益统计构造

#参数:

#输入:开始时间,结束时间,股票池,计算天数

pool = get_index_stocks('000300.XSHG')

start_d='2016-5-9'

end_d='2018-5-10'

days = 1

def get_pool_pct(pool,start_date,end_date,days=1):

df_sh50 = get_price(pool,start_date=start_d,end_date=end_d,fields=['close'])['close']

pct_close = (df_sh50[days:].values-df_sh50[:-days].values)/df_sh50[:-days].values

df_temp = df_sh50#.ix[1:,:]

df_temp.iloc[days:,:]=pct_close

df_temp.iloc[0:days,:] = np.nan

return df_temp

factor_return = get_pool_pct(pool=pool,start_date=start_d,end_date=end_d,days=days)

#计算因子IC值,P值

#输入:因子序列和收益序列

#返回IC和IR

#注意事项:输入的是df格式内容,函数会剔除空值

def get_rank_ic(factor, factor_return,days = 1):

ic_df = pd.DataFrame(index=factor.index, columns=['IC','pValue'])

# 计算相关系数

date_index = factor.index

for i in range(len(date_index)-days):

tmp_factor = factor.ix[date_index[i]]

tmp_ret = factor_return.ix[date_index[i+days]]

cor = pd.DataFrame(tmp_factor)

ret = pd.DataFrame(tmp_ret)

cor.columns = ['corr']

ret.columns = ['ret']

cor['ret'] = ret['ret']

#去除空值

cor = cor[~pd.isnull(cor['corr'])][~pd.isnull(cor['ret'])]

ic, p_value = st.spearmanr(cor['corr'], cor['ret']) # 计算秩相关系数RankIC

ic_df['IC'][i] = ic

ic_df['pValue'][i] = p_value

return ic_df

#因子数据获取比较耗时,这里直接读取的已经存在本地的CSV文件

alpha_001_factor = pd.read_csv('alpha_001.csv')

alpha_001_factor_neu = pd.read_csv('alpha_001_neu.csv')

alpha_001_factor.index = alpha_001_factor.iloc[:,0]

alpha_001_factor_neu.index = alpha_001_factor_neu.iloc[:,0]

#用于计算不同周期的信息系数

factor_ic = {}

factor_neu_ic = {}

for i in range(5):

ic_alpha_day=get_rank_ic(alpha_001_factor,factor_return,days=i+1)

ic_alpha_neu_day=get_rank_ic(alpha_001_factor_neu,factor_return,days=i+1)

factor_ic[str(i+1)+'day']=ic_alpha_day

factor_neu_ic[str(i+1)+'day']=ic_alpha_neu_day

factor_ic

/opt/conda/envs/python2new/lib/python2.7/site-packages/ipykernel_launcher.py:10: DeprecationWarning: .ix is deprecated. Please use .loc for label based indexing or .iloc for positional indexing See the documentation here: http://pandas.pydata.org/pandas-docs/stable/indexing.html#ix-indexer-is-deprecated # Remove the CWD from sys.path while we load stuff. /opt/conda/envs/python2new/lib/python2.7/site-packages/ipykernel_launcher.py:11: DeprecationWarning: .ix is deprecated. Please use .loc for label based indexing or .iloc for positional indexing See the documentation here: http://pandas.pydata.org/pandas-docs/stable/indexing.html#ix-indexer-is-deprecated # This is added back by InteractiveShellApp.init_path() /opt/conda/envs/python2new/lib/python2.7/site-packages/ipykernel_launcher.py:18: UserWarning: Boolean Series key will be reindexed to match DataFrame index.

{'1day': IC pValue

0 -0.0325512 0.599225

1 -0.0462635 0.454143

2 0.103766 0.0930901

3 0.0847722 0.168838

4 -0.143398 0.0197563

5 0.211088 0.000555462

6 0.0305919 0.621398

7 0.0294278 0.633442

8 -0.110679 0.0709847

9 0.144478 0.0181706

10 0.0479846 0.433161

11 0.158497 0.00948303

12 -0.000761458 0.990119

13 0.128105 0.0367893

14 0.0693315 0.258927

15 -0.0968994 0.11283

16 0.250729 3.07897e-05

17 -0.0564929 0.353327

18 -0.0208197 0.733441

19 0.135 0.0262632

20 -0.106695 0.0795483

21 0.0155223 0.799214

22 -0.0427796 0.482298

23 0.0270633 0.656184

24 -0.174528 0.0037552

25 -0.0578074 0.343117

26 0.101989 0.0932154

27 0.0571404 0.346935

28 0.159334 0.00872218

29 -0.129137 0.033591

.. ... ...

458 0.0832798 0.154347

459 0.172722 0.00316892

460 0.0422972 0.472294

461 0.228711 8.48727e-05

462 0.0304881 0.605107

463 0.0965626 0.100769

464 0.0323553 0.583173

465 0.15357 0.0089252

466 -0.0422501 0.473556

467 0.0813818 0.167653

468 -0.044024 0.455169

469 0.128974 0.0280895

470 0.00488431 0.934111

471 0.313418 5.24586e-08

472 -0.0320121 0.587828

473 -0.17822 0.00231676

474 0.131821 0.0247715

475 0.0630512 0.284551

476 0.12994 0.0266594

477 0.0782491 0.183148

478 0.16528 0.00477412

479 0.0440963 0.456791

480 0.0146184 0.804561

481 0.032384 0.583495

482 -0.0199018 0.735751

483 0.0845603 0.15019

484 0.0477487 0.417894

485 0.183121 0.00173919

486 0.0248344 0.673109

487 NaN NaN

[488 rows x 2 columns], '2day': IC pValue

0 -0.0629855 0.308869

1 0.0198755 0.747878

2 0.079178 0.200564

3 -0.141565 0.0211529

4 0.233844 0.000125669

5 0.173071 0.00480188

6 0.0349641 0.572418

7 -0.0021884 0.971716

8 0.152491 0.0126082

9 0.021518 0.72634

10 0.156411 0.0101929

11 -0.0673022 0.273162

12 0.1638 0.00731627

13 0.0759822 0.216763

14 -0.242812 6.09426e-05

15 0.0844765 0.167114

16 -0.0776523 0.203388

17 0.0920267 0.130034

18 0.162318 0.00752811

19 -0.116289 0.0558751

20 0.00970124 0.873694

21 -0.0527188 0.387341

22 0.0515109 0.397447

23 -0.166853 0.00571641

24 -0.0833905 0.168684

25 0.104897 0.084781

26 0.0603345 0.321499

27 0.192409 0.00140106

28 -0.11282 0.0641506

29 0.0990213 0.10383

.. ... ...

458 0.0423907 0.469018

459 0.0692149 0.239992

460 0.267111 3.81523e-06

461 -0.0162369 0.783064

462 0.124293 0.0343708

463 -0.0438933 0.456509

464 0.0782272 0.184031

465 -0.0684607 0.245988

466 0.0939277 0.110455

467 0.00798227 0.892523

468 0.104767 0.0748599

469 0.0106916 0.856139

470 0.293568 3.74613e-07

471 -0.168142 0.00415099

472 -0.150847 0.0102287

473 0.101955 0.0830516

474 0.0101044 0.863962

475 0.125128 0.0331688

476 0.0771821 0.18921

477 0.00400974 0.945701

478 -0.0771689 0.190054

479 0.0642117 0.278282

480 0.066898 0.256959

481 0.103991 0.0775675

482 0.0245137 0.67762

483 -0.00366654 0.950342

484 0.173249 0.00307637

485 0.0147688 0.802254

486 NaN NaN

487 NaN NaN

[488 rows x 2 columns], '3day': IC pValue

0 -0.0243898 0.693794

1 0.0575214 0.35188

2 -0.174327 0.00457712

3 0.226679 0.00019829

4 0.130043 0.0346948

5 -0.117311 0.0569601

6 0.00459606 0.940866

7 0.0695949 0.258925

8 0.0287341 0.640205

9 0.0953753 0.120023

10 -0.0567579 0.353765

11 0.199031 0.00107658

12 -0.0785902 0.2005

13 -0.214921 0.000415413

14 -0.0256282 0.676772

15 -0.109539 0.0728754

16 0.101877 0.0948025

17 0.189131 0.0017292

18 -0.179547 0.0030698

19 0.032276 0.596797

20 -0.085082 0.162508

21 0.00209657 0.972595

22 -0.110198 0.0695866

23 -0.129295 0.0327219

24 0.0636558 0.293746

25 0.012542 0.837165

26 0.21222 0.000424884

27 -0.11632 0.0549055

28 0.152135 0.0123209

29 0.163869 0.00686233

.. ... ...

458 0.0610033 0.297178

459 0.260211 7.1331e-06

460 0.00543286 0.926476

461 0.145794 0.0129423

462 -0.0671292 0.254487

463 -0.0551603 0.349273

464 -0.134219 0.0222455

465 0.115088 0.0506393

466 -0.0259631 0.659719

467 0.0255725 0.665073

468 -0.0396878 0.500817

469 0.176078 0.00262023

470 -0.136145 0.0206003

471 -0.120208 0.0411429

472 0.0996164 0.0909617

473 0.0822764 0.162283

474 0.178643 0.00226087

475 0.0769109 0.191544

476 0.00962391 0.870149

477 0.0148943 0.80027

478 0.0781048 0.184721

479 0.0749081 0.205777

480 0.0856011 0.146619

481 -0.0162343 0.783466

482 -0.0259744 0.659581

483 0.107978 0.0658541

484 0.0377491 0.521981

485 NaN NaN

486 NaN NaN

487 NaN NaN

[488 rows x 2 columns], '4day': IC pValue

0 0.0819587 0.185156

1 -0.233889 0.000125286

2 0.287934 2.0523e-06

3 0.180741 0.00315016

4 -0.116255 0.0592476

5 0.0195204 0.752234

6 0.00260236 0.966497

7 0.0133127 0.829222

8 0.0238694 0.697828

9 -0.0389373 0.52641

10 0.150864 0.0132485

11 -0.0772188 0.208492

12 -0.23246 0.00012646

13 -0.0544847 0.376107

14 -0.199733 0.00103263

15 0.16151 0.00795278

16 0.23563 9.26727e-05

17 -0.172575 0.0043101

18 0.0698632 0.252606

19 -0.106854 0.0790988

20 0.0329688 0.588939

21 0.123957 0.0414467

22 -0.167655 0.00557228

23 0.149146 0.0136323

24 -0.0523312 0.38821

25 0.194876 0.00126324

26 -0.0716961 0.238592

27 0.111941 0.0647636

28 0.149928 0.0136593

29 -0.0749464 0.218772

.. ... ...

458 0.290341 4.04833e-07

459 0.0266132 0.651753

460 0.131094 0.0253306

461 -0.0203115 0.73052

462 -0.0320176 0.587112

463 -0.0653113 0.267607

464 0.0862965 0.142658

465 0.0124458 0.833145

466 0.0736355 0.211208

467 -0.0767864 0.193042

468 0.0641485 0.276237

469 -0.105269 0.0734692

470 -0.0958584 0.103891

471 0.0483174 0.413178

472 0.0425572 0.471117

473 -0.0402118 0.495175

474 0.0279847 0.635074

475 -0.0374525 0.525257

476 -0.0389268 0.508333

477 0.147726 0.0116347

478 0.083015 0.158532

479 0.0645822 0.275512

480 -0.00921437 0.876058

481 -0.0877411 0.136749

482 0.119245 0.0424443

483 0.0142805 0.808337

484 NaN NaN

485 NaN NaN

486 NaN NaN

487 NaN NaN

[488 rows x 2 columns], '5day': IC pValue

0 -0.218641 0.000354007

1 0.163391 0.0078119

2 0.169402 0.00588551

3 -0.121945 0.0473518

4 0.129282 0.0357793

5 -0.155612 0.0113464

6 0.0517323 0.403424

7 0.153341 0.0124473

8 -0.0843436 0.169389

9 0.117874 0.0543864

10 0.00933894 0.878824

11 -0.227008 0.000183363

12 0.0447693 0.466327

13 -0.0897818 0.144194

14 0.214596 0.000413529

15 0.0779474 0.202515

16 -0.229252 0.000144552

17 -0.013081 0.82996

18 -0.0408444 0.503938

19 -0.0392211 0.520273

20 0.158865 0.00879768

21 -0.165627 0.00627862

22 0.143717 0.0177089

23 -0.124786 0.03936

24 0.198115 0.000976773

25 -0.0566564 0.352828

26 0.110207 0.0695624

27 0.155191 0.0102289

28 -0.149911 0.0136705

29 -0.0131562 0.82931

.. ... ...

458 -0.0480161 0.412062

459 0.103316 0.079

460 -0.01675 0.776009

461 -0.0888995 0.130952

462 -0.0843498 0.151922

463 0.0200563 0.733778

464 -0.0713412 0.225821

465 0.0229844 0.697208

466 -0.163141 0.00535486

467 0.0428611 0.467952

468 -0.00172116 0.976718

469 -0.194136 0.000889246

470 0.00796346 0.892775

471 0.080842 0.170499

472 0.0270098 0.647484

473 -0.0215971 0.714186

474 -0.0394058 0.503867

475 -0.0497814 0.398329

476 0.0972651 0.0977208

477 0.148836 0.0110156

478 0.0507965 0.388768

479 0.0247429 0.676382

480 -0.192798 0.000986613

481 0.0492726 0.403993

482 -0.0295379 0.616407

483 NaN NaN

484 NaN NaN

485 NaN NaN

486 NaN NaN

487 NaN NaN

[488 rows x 2 columns]}

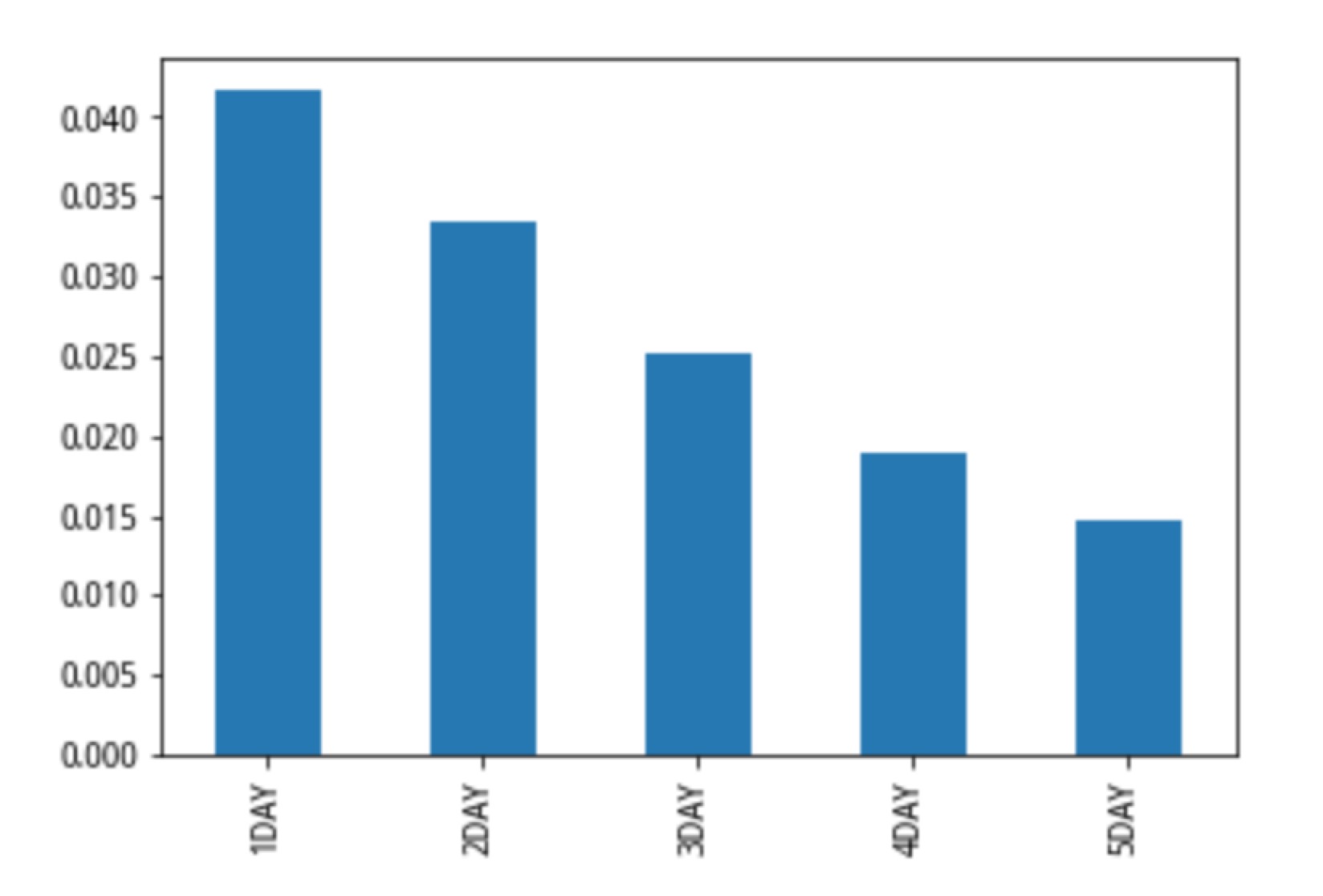

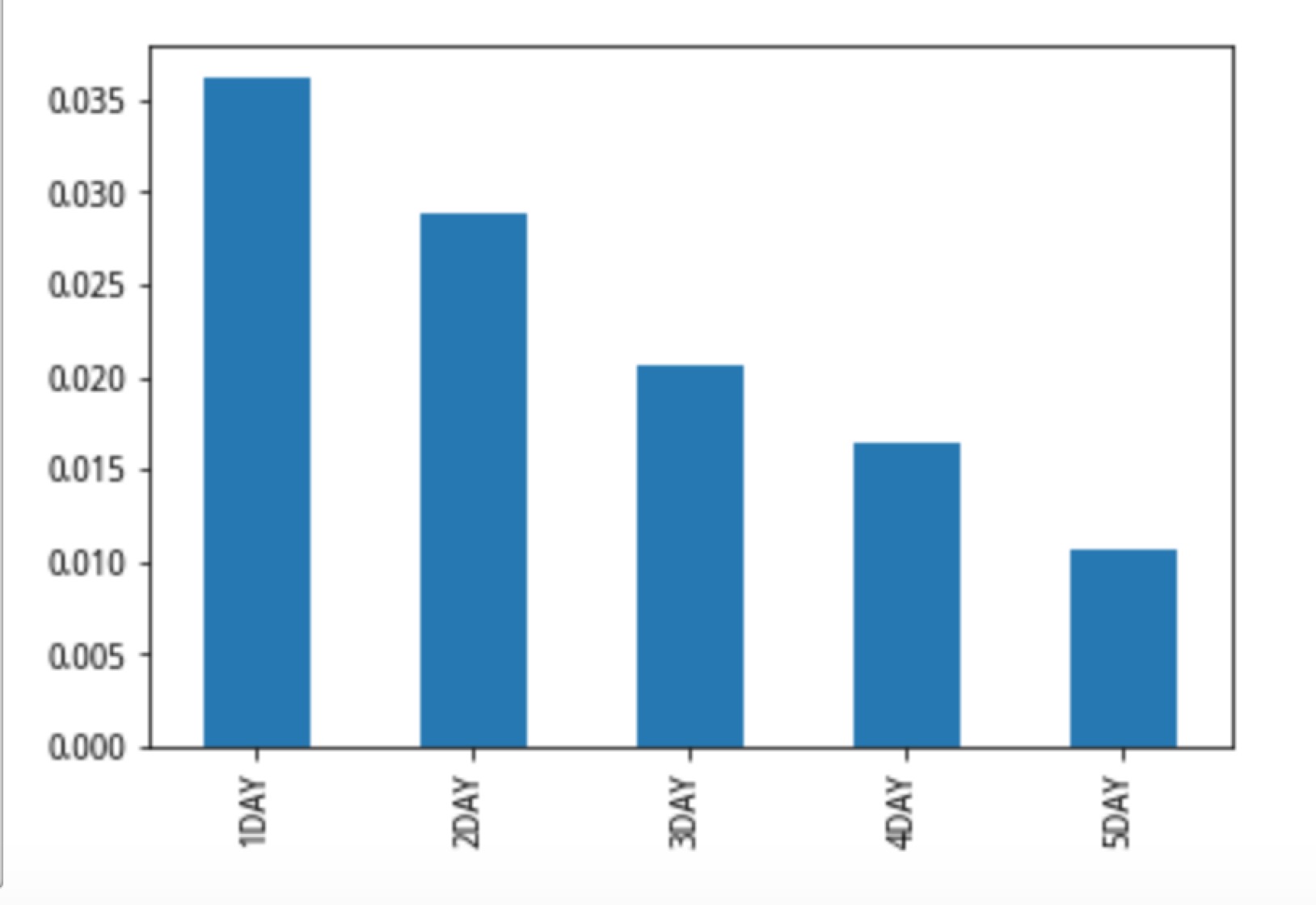

alpha_report = pd.DataFrame(index=['1DAY', '2DAY', '3DAY','4DAY','5DAY'],

columns=[['alpha_001因子','alpha_001因子','alpha_001因子', '行业和市值中性化后因子', '行业和市值中性化后因子','行业和市值中性化后因子'],

['IC', 'IC_IR', 'pvalue', 'IC', 'IC_IR', 'pvalue']])

for i in range(1,6):

l = [factor_ic[str(i)+'day']['IC'].mean(),factor_ic[str(i)+'day']['IC'].mean()/factor_ic[str(i)+'day']['IC'].std(),factor_ic[str(i)+'day']['pValue'].mean()]

l_neu = [factor_neu_ic[str(i)+'day']['IC'].mean(),factor_neu_ic[str(i)+'day']['IC'].mean()/factor_neu_ic[str(i)+'day']['IC'].std(),factor_neu_ic[str(i)+'day']['pValue'].mean()]

alpha_report.loc[str(i)+'DAY',:] = l+l_neu

alpha_report

| alpha_001因子 | 行业和市值中性化后因子 | |||||

|---|---|---|---|---|---|---|

| IC | IC_IR | pvalue | IC | IC_IR | pvalue | |

| 1DAY | 0.0417148 | 0.321501 | 0.261799 | 0.0362106 | 0.419845 | 0.378196 |

| 2DAY | 0.033475 | 0.264444 | 0.292318 | 0.0289102 | 0.348966 | 0.392869 |

| 3DAY | 0.0252228 | 0.203112 | 0.314084 | 0.0206561 | 0.250984 | 0.39676 |

| 4DAY | 0.0189274 | 0.154679 | 0.32307 | 0.0164229 | 0.20391 | 0.406601 |

| 5DAY | 0.0146902 | 0.123258 | 0.302474 | 0.010626 | 0.131947 | 0.397704 |

alpha_report['alpha_001因子']['IC'].plot(kind='bar')

<matplotlib.axes._subplots.AxesSubplot at 0x7f8ff699d3d0>

alpha_report['行业和市值中性化后因子']['IC'].plot(kind='bar')

<matplotlib.axes._subplots.AxesSubplot at 0x7f8ff69bec50>

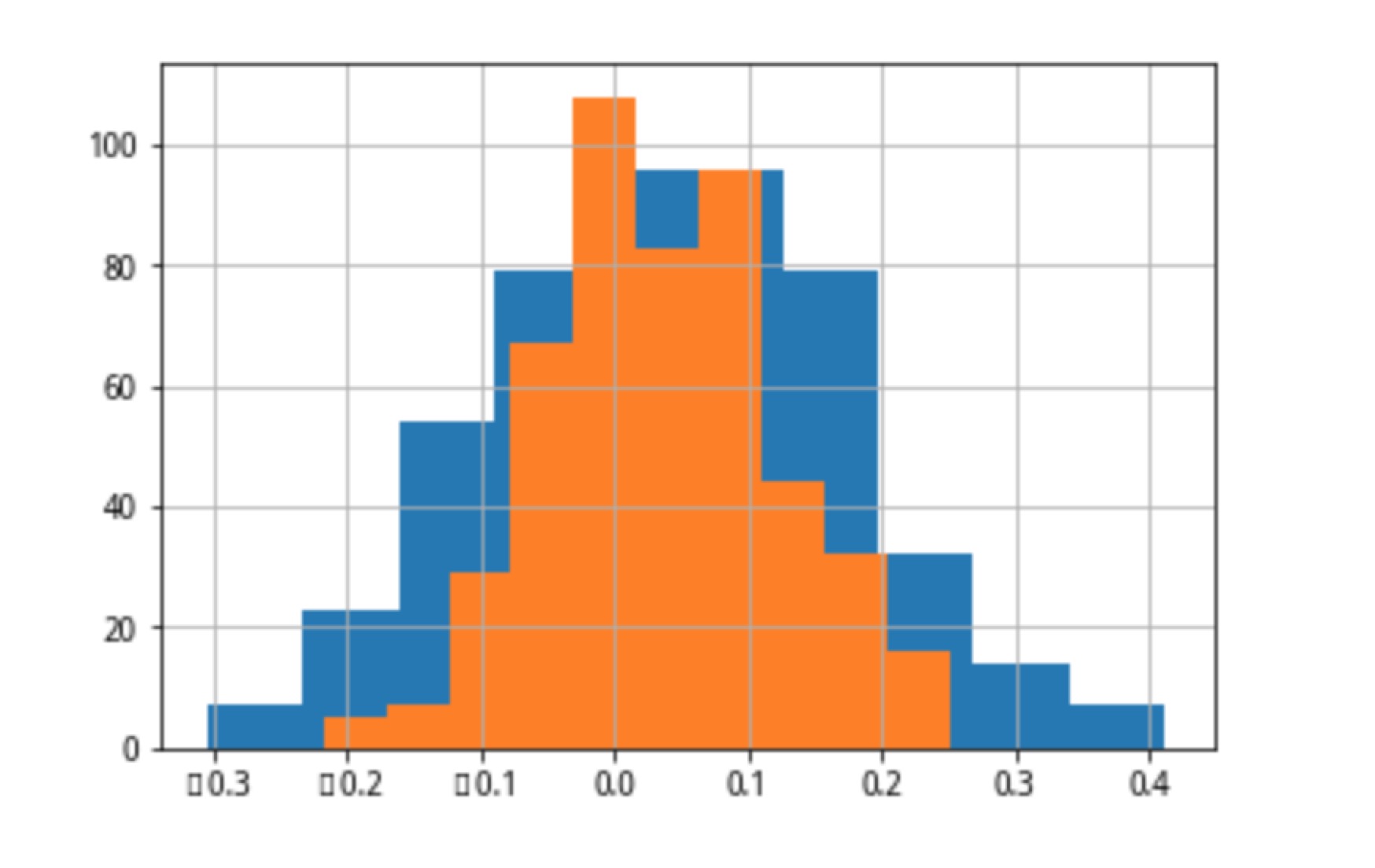

factor_ic['1day']['IC'].hist(),factor_neu_ic['1day']['IC'].hist()

(<matplotlib.axes._subplots.AxesSubplot at 0x7f9005840350>, <matplotlib.axes._subplots.AxesSubplot at 0x7f9005840350>)

factor_ic['1day']['IC'].plot(),factor_neu_ic['1day']['IC'].plot()

(<matplotlib.axes._subplots.AxesSubplot at 0x7f8ff68f4950>, <matplotlib.axes._subplots.AxesSubplot at 0x7f8ff68f4950>)

factor_ic['2day']['IC'].hist(),factor_neu_ic['2day']['IC'].hist()

(<matplotlib.axes._subplots.AxesSubplot at 0x7f9005de3e90>, <matplotlib.axes._subplots.AxesSubplot at 0x7f9005de3e90>)

factor_ic['3day']['IC'].hist(),factor_neu_ic['3day']['IC'].hist()

(<matplotlib.axes._subplots.AxesSubplot at 0x7f9001d5ed10>, <matplotlib.axes._subplots.AxesSubplot at 0x7f9001d5ed10>)

factor_ic['4day']['IC'].hist(),factor_neu_ic['4day']['IC'].hist()

(<matplotlib.axes._subplots.AxesSubplot at 0x7f90015821d0>, <matplotlib.axes._subplots.AxesSubplot at 0x7f90015821d0>)

factor_ic['5day']['IC'].hist(),factor_neu_ic['5day']['IC'].hist()

(<matplotlib.axes._subplots.AxesSubplot at 0x7f8ffc1a2410>, <matplotlib.axes._subplots.AxesSubplot at 0x7f8ffc1a2410>)

#按因子值进行收益分组统计

#定义一个大函数

import pandas as pd

import numpy as np

#import matplotlib.pyplot as plt

#plt.style.use('ggplot')

def get_fact_ret(fact,pool_index='000300.XSHG',fdate='2017-01-01',e_date='2017-02-01'):

def get_df(pool,fdate):

q = query(

valuation.code,

valuation.circulating_market_cap,

valuation.pe_ratio,

valuation.pe_ratio/indicator.inc_net_profit_year_on_year,

valuation.pb_ratio

).filter(

valuation.code.in_(pool))

df = get_fundamentals(q, fdate)

df.columns=['code','circulating_market_cap','pe_ratio','peg','pb_ratio']

#print(df)

return df

def ret_se(sl,start_date=fdate,end_date=e_date):

#得到股票的历史价格数据

df = get_price(sl,start_date=start_date,end_date=end_date,fields=['close']).close

df = df.dropna(axis=1)

#print(df.head(3))

#相当于昨天的百分比变化

pct = df.pct_change()+1

pct.ix[0,:] = 1

#pct = pct.dropna(axis=0)

#累积相乘得到总收益的变化情况

#df1 = pct.cumprod()

#等权重平均收益结果

se1 = pct.cumsum(axis=1).ix[:,-1]/pct.shape[1]

return se1

'''

#获取因子值,进行排序

pool = get_index_stocks(pool_index)

df = get_df(pool,fdate=fdate)

df.index = df.code

'''

df_d1 = fact.loc[fdate:fdate,:].T.sort_values(fdate,ascending=0)[1:]

#print(df_d1.head(3))

#step2 分组

part = list(df_d1.index)

a = len(df_d1)//5

part1 = list(df_d1.index)[:a]

part2 = list(df_d1.index)[a:2*a]

part3 = list(df_d1.index)[2*a:-2*a]

part4 = list(df_d1.index)[-2*a:-a]

part5 = list(df_d1.index)[-a:]

#step3 计算收益

se = ret_se(part)

se1 = ret_se(part1)

se2 = ret_se(part2)

se3 = ret_se(part3)

se4 = ret_se(part4)

se5 = ret_se(part5)

return se,se1,se2,se3,se4,se5

#数据组拼接

def fact_tu(fact,l_all):

l1 = l_all[:-1]

l2 = l_all[1:]

date_list = list(zip(l1,l2))

num = 1

for i,j in date_list:

se,se1,se2,se3,se4,se5 = get_fact_ret(fact,fdate=i,e_date=j)

if num == 1:

#se_list = [ for i in se_list]

df_all_1 = pd.concat([se,se1,se2,se3,se4,se5],axis=1)

df_all_1.columns = ['benchmark','part1','part2','part3','part4','part5']

#df_all_1.ix[0,:] = 1

num = 0

#print(df_all_1)

else:

df_all_2 = pd.concat([se,se1,se2,se3,se4,se5],axis=1)

df_all_2.columns = ['benchmark','part1','part2','part3','part4','part5']

#df_all_2.ix[0,:] = 1

#将各个月份的收益拼接为大表

df_all_1 = pd.concat([df_all_1,df_all_2])

#print(df_all_1)

return df_all_1.cumprod()

#获取时间段内的月初首个交易日日期

#获取每个月的第一个交易日日期

'''

def date_list(start,end):

df_date = pd.read_csv('df_date.csv')

df_1=df_date[(df_date['dt_list']>=start) & (df_date['dt_list']<=end) ]

df_2 = df_1.drop_duplicates(['year','month'])

l_3 = [i for i in df_2.dt_list.values]

return l_3

'''

#每天进行调仓

def date_list(start,end):

l1 = get_price('000001.XSHG',start_date=start,end_date=end)

l2 = [str(i)[:10] for i in l1.index]

return l2

#输入起止日期

l_date=date_list('2017-05-10','2018-05-10')

#输入目标因子进行分组测试

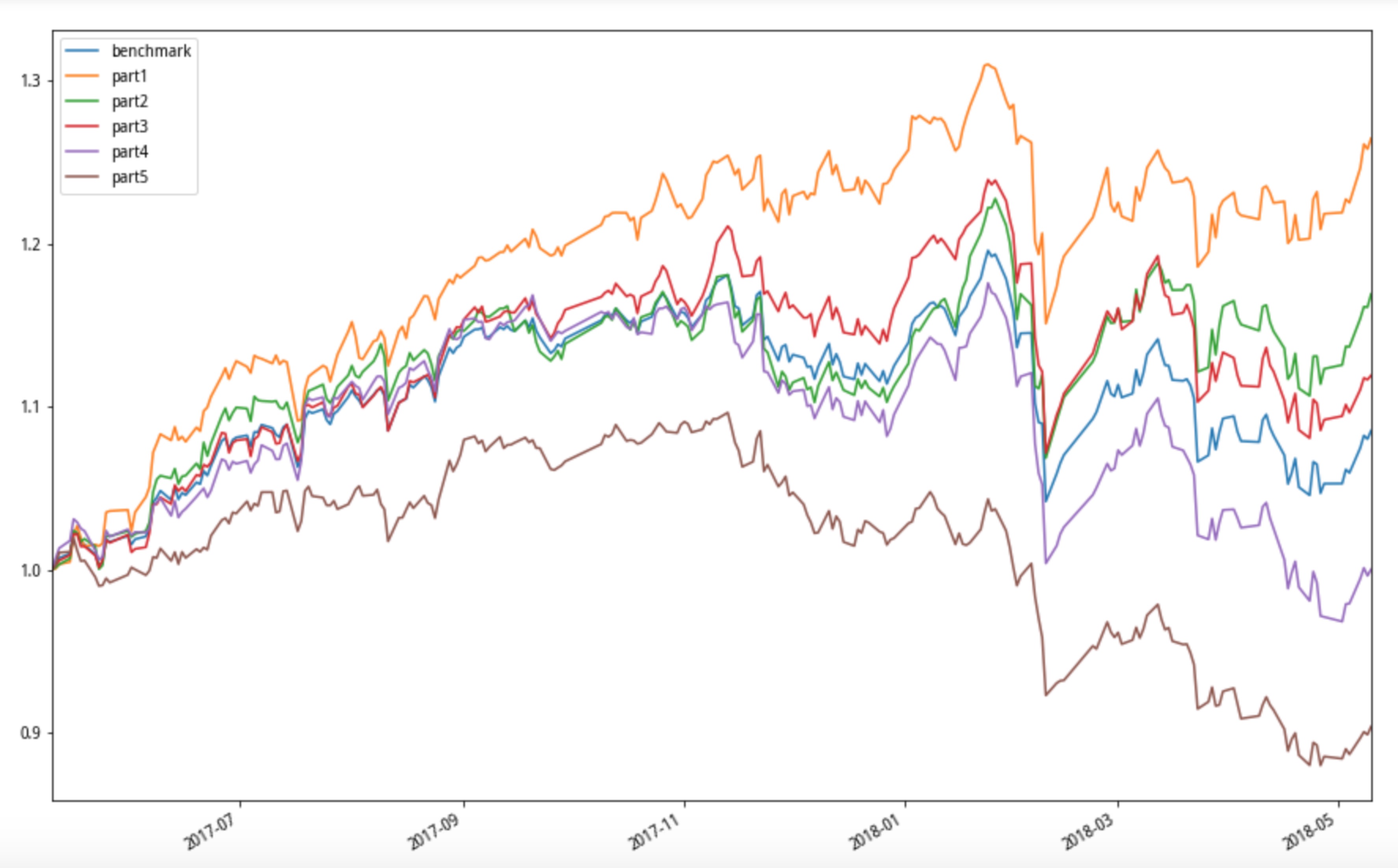

df = fact_tu(alpha_001_factor,l_date)

#对分组收益进行制图

df.plot(figsize=(15,10))

/opt/conda/envs/python2new/lib/python2.7/site-packages/ipykernel_launcher.py:31: DeprecationWarning: .ix is deprecated. Please use .loc for label based indexing or .iloc for positional indexing See the documentation here: http://pandas.pydata.org/pandas-docs/stable/indexing.html#ix-indexer-is-deprecated /opt/conda/envs/python2new/lib/python2.7/site-packages/ipykernel_launcher.py:36: DeprecationWarning: .ix is deprecated. Please use .loc for label based indexing or .iloc for positional indexing See the documentation here: http://pandas.pydata.org/pandas-docs/stable/indexing.html#ix-indexer-is-deprecated

<matplotlib.axes._subplots.AxesSubplot at 0x7f8ff6517450>

#输入起止日期

l_date=date_list('2017-05-10','2018-05-10')

#输入目标因子进行分组测试

df = fact_tu(alpha_001_factor_neu,l_date)

#对分组收益进行制图

df.plot(figsize=(15,10))

/opt/conda/envs/python2new/lib/python2.7/site-packages/ipykernel_launcher.py:31: DeprecationWarning: .ix is deprecated. Please use .loc for label based indexing or .iloc for positional indexing See the documentation here: http://pandas.pydata.org/pandas-docs/stable/indexing.html#ix-indexer-is-deprecated /opt/conda/envs/python2new/lib/python2.7/site-packages/ipykernel_launcher.py:36: DeprecationWarning: .ix is deprecated. Please use .loc for label based indexing or .iloc for positional indexing See the documentation here: http://pandas.pydata.org/pandas-docs/stable/indexing.html#ix-indexer-is-deprecated

<matplotlib.axes._subplots.AxesSubplot at 0x7f8ff4bb3f10>

本社区仅针对特定人员开放

查看需注册登录并通过风险意识测评

5秒后跳转登录页面...