简介

在下单函数后调用 write_logs(contest),将order、trade、position对象,以csv格式输出三张表至研究,新的数据将追加在数据框后,在回测和模拟交易中均可使用。支持每日、分钟策略保存对象,分为每日定时调用保存函数和按order调用保存函数,若分钟级策略按order调用时,可能由于下单数量过多导致回测速度下降,建议使用定时调用保存函数。本篇使用官网回测环境,给出期货每日定时调用保存函数的简单实例,文件输出在研究根目录下,若使用客户端请自行在根目录中寻找文件。

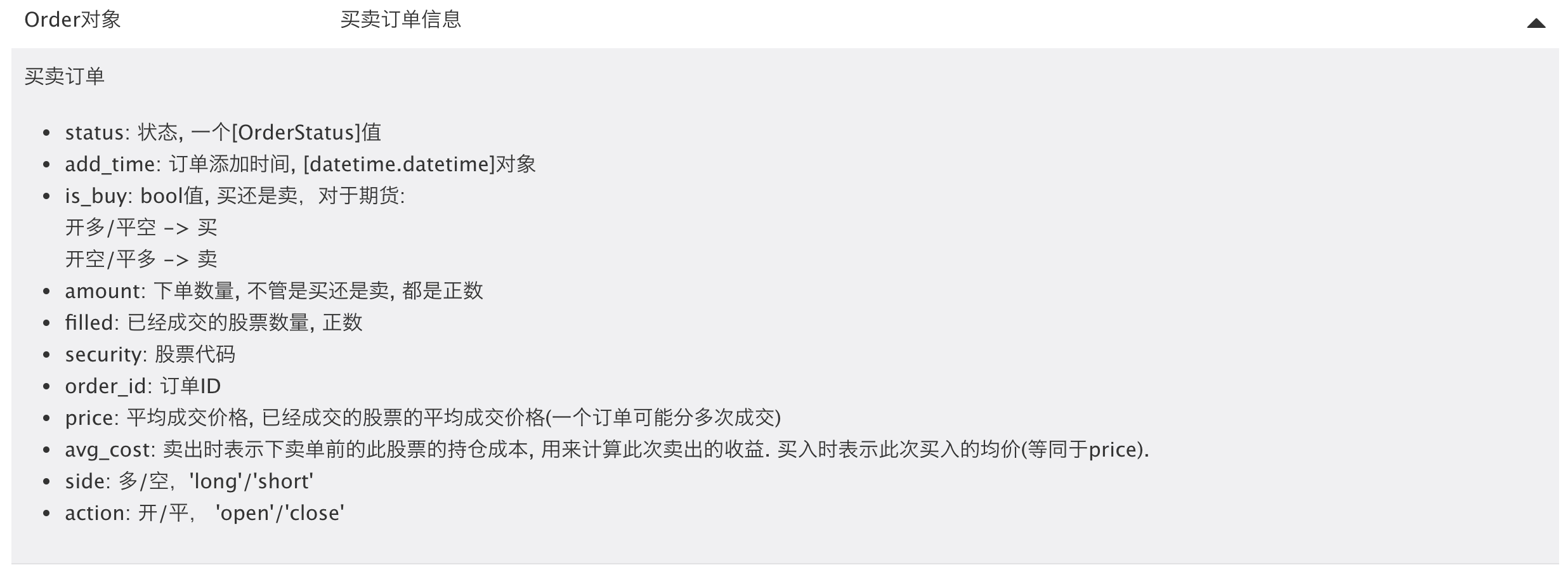

Order

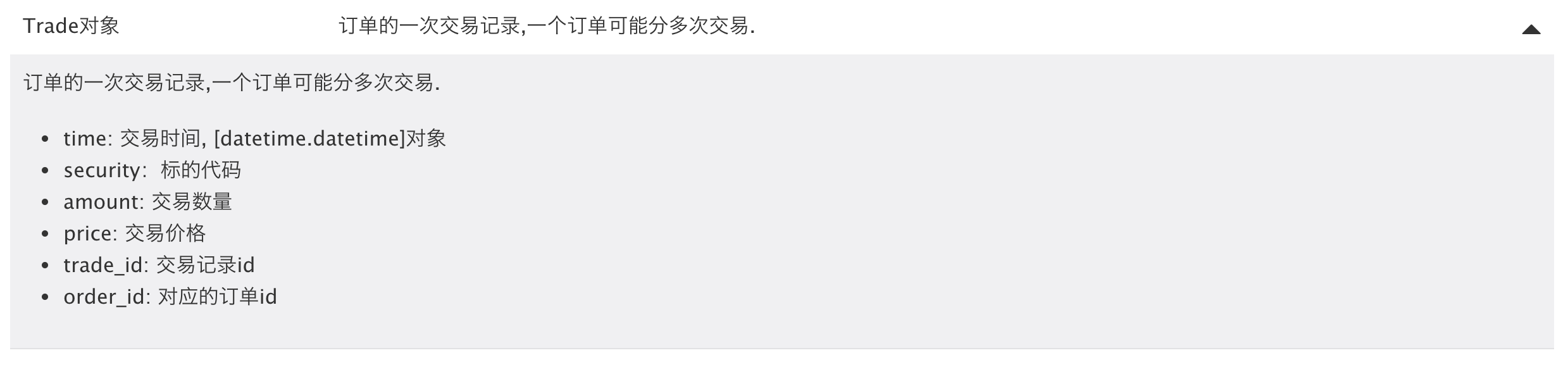

Trade

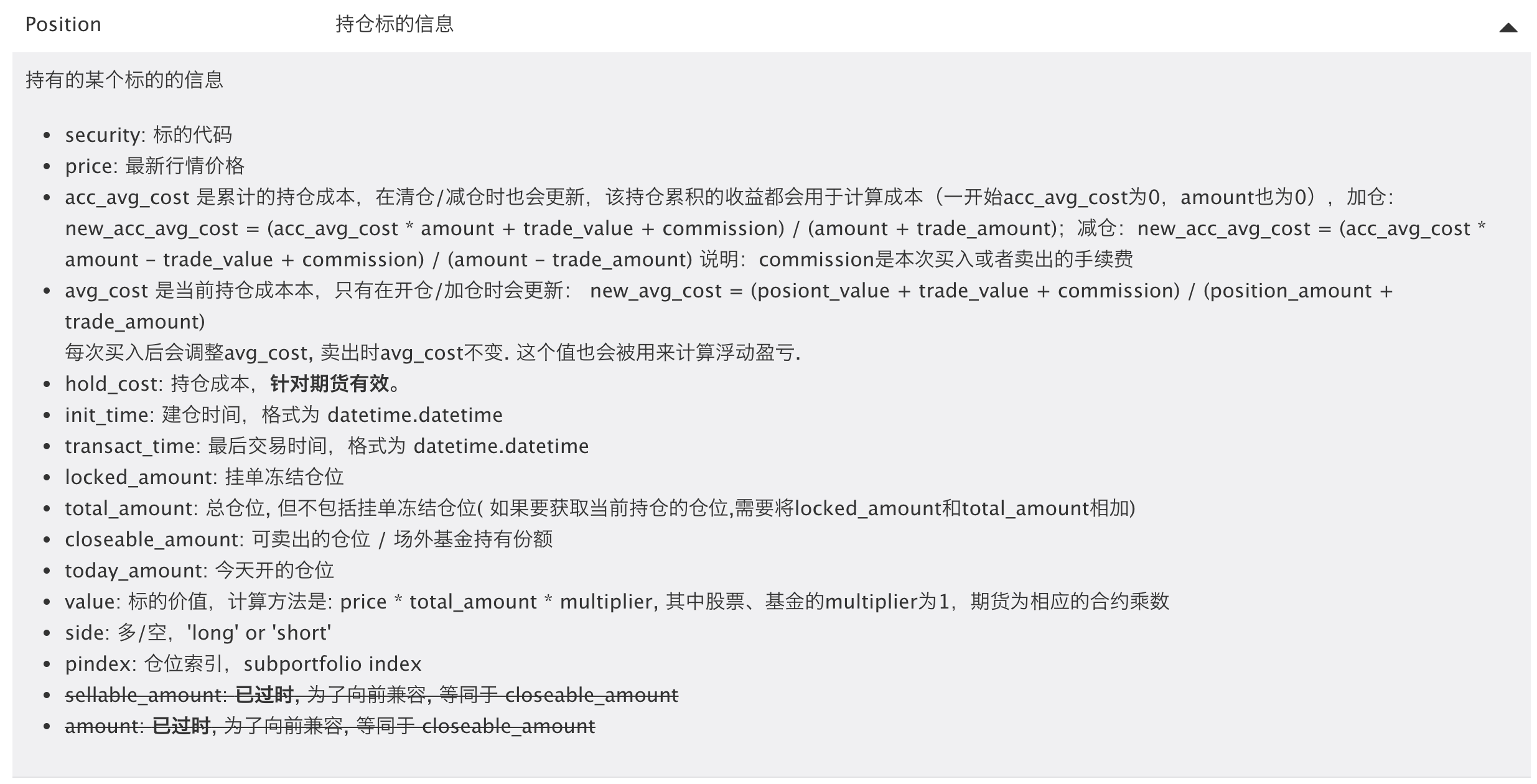

Position

def process_initialize(context):

ls=['security']

g.__df1 = pd.DataFrame(columns=ls)

g.__df2 = pd.DataFrame(columns=ls)

g.__df3 = pd.DataFrame(columns=ls)

def write_logs(context):

orders = get_orders()

i=0

ls1 = ['order_id','status','security','price','amount',\

'avg_cost','Time','is_buy','filled','side','action']

df1 = pd.DataFrame(columns=ls1)

for _orders in orders.values():

df1.loc[i,'order_id'] = _orders.order_id

df1.loc[i,'status'] = _orders.status

df1.loc[i, 'security'] = _orders.security

df1.loc[i,'price'] = _orders.price

df1.loc[i,'amount'] = _orders.amount

df1.loc[i,'avg_cost'] = _orders.avg_cost

df1.loc[i, 'Time'] = _orders.add_time

df1.loc[i, 'is_buy'] = _orders.is_buy

df1.loc[i, 'filled'] = _orders.filled

df1.loc[i, 'side'] = _orders.side

df1.loc[i, 'action'] = _orders.action

i=i 1

df1.set_index('Time',drop=True,inplace=True)

g.__df1 = g.__df1.append(df1)

write_file('orders.csv', g.__df1.to_csv())

trades = get_trades()

i=0

ls2 = ['Time','order_id','trade_id','security','price','amount']

df2 = pd.DataFrame(columns=ls2)

for _trades in trades.values():

df2.loc[i,'Time'] = _trades.time

df2.loc[i,'order_id'] = _trades.order_id

df2.loc[i, 'trade_id'] = _trades.trade_id

df2.loc[i,'security'] = _trades.security

df2.loc[i,'price'] = _trades.price

df2.loc[i,'amount'] = _trades.amount

i=i 1

df2.set_index('Time',drop=True,inplace=True)

g.__df2 = g.__df2.append(df2)

write_file('trade.csv', g.__df2.to_csv())

position = context.portfolio.positions.keys()

i=0

ls3 = ['security','price','acc_avg_cost','avg_cost','Time','transact_time','total_amount',\

'closeable_amount','today_amount','locked_amount','value','side']

df3 = pd.DataFrame(columns=ls3)

for stock in position:

df3.loc[i,'security']=context.portfolio.positions[stock].security

df3.loc[i,'price'] = context.portfolio.positions[stock].price

df3.loc[i,'acc_avg_cost'] = context.portfolio.positions[stock].acc_avg_cost

df3.loc[i,'avg_cost'] = context.portfolio.positions[stock].avg_cost

df3.loc[i, 'Time'] = context.portfolio.positions[stock].init_time

df3.loc[i,'transact_time'] = context.portfolio.positions[stock].transact_time

df3.loc[i,'total_amount'] = context.portfolio.positions[stock].total_amount

df3.loc[i,'closeable_amount'] = context.portfolio.positions[stock].closeable_amount

df3.loc[i,'today_amount'] = context.portfolio.positions[stock].today_amount

df3.loc[i,'locked_amount'] = context.portfolio.positions[stock].locked_amount

df3.loc[i,'value'] = context.portfolio.positions[stock].value

df3.loc[i,'side'] = context.portfolio.positions[stock].side

i=i 1

df3.set_index('Time',drop=True,inplace=True)

g.__df3 = g.__df3.append(df3)

write_file('Position.csv', g.__df3.to_csv())